Baltimore: Health Insurance Market Primed for National Health Reform

RWJF Reform Community Report

May 2013

Laurie E. Felland, Chapin White, Amanda E. Lechner, Rebecca Gourevitch

![]() ith a history of aggressive state oversight of health care and Medicaid coverage expansions, the Baltimore metropolitan area likely faces a smoother transition to national health reform than many other markets across the country, according to a new Center for Studying Health System Change (HSC) study of the region’s commercial and Medicaid insurance markets (see Data Source). In large part, Maryland’s implementation of health reform may be easier because the state previously enacted requirements similar to the Patient Protection and Affordable Care Act of 2010 (ACA), including small-group insurance market reforms and Medicaid coverage expansions for low-income people without children. Since national health reform’s passage in 2010, Maryland Gov. Martin O’Malley (D) and the state Legislature have embraced other reform goals, including creation of a state-based health insurance exchange. Key factors likely to influence how national health reform plays out in the Baltimore area include:

ith a history of aggressive state oversight of health care and Medicaid coverage expansions, the Baltimore metropolitan area likely faces a smoother transition to national health reform than many other markets across the country, according to a new Center for Studying Health System Change (HSC) study of the region’s commercial and Medicaid insurance markets (see Data Source). In large part, Maryland’s implementation of health reform may be easier because the state previously enacted requirements similar to the Patient Protection and Affordable Care Act of 2010 (ACA), including small-group insurance market reforms and Medicaid coverage expansions for low-income people without children. Since national health reform’s passage in 2010, Maryland Gov. Martin O’Malley (D) and the state Legislature have embraced other reform goals, including creation of a state-based health insurance exchange. Key factors likely to influence how national health reform plays out in the Baltimore area include:

- Hospital rate regulation effects on market dynamics. For several decades, Maryland through a rate-setting system has regulated hospital payment rates for Medicare, Medicaid and private payers. Because of this system, Maryland hospital spending on average has grown more slowly historically than the nation as a whole. However, similar to many other markets, Baltimore-area hospital systems are acquiring independent hospitals and employing physicians to gain patients and higher revenues.

- Little innovation to control employer-based insurance costs. While commercial coverage is considered relatively comprehensive overall, employersŌĆöparticularly small firmsŌĆöhave placed more cost-sharing responsibility on employees and increasingly adopted lower-cost, high-deductible health plans. While interested in wellness activities and limited-provider networks to control costs, employers reportedly have been slow to innovate in terms of insurance product design.

- CareFirst BlueCross BlueShield dominance of the commercial market. Regional CareFirst BlueCross BlueShield is the largest commercial insurerŌĆöparticularly in the individual and small-group marketsŌĆöwith remaining market share divided among national carriers, including UnitedHealth Group, Aetna, CIGNA and Kaiser Permanente.

- Significant insurer interest in Medicaid. Health plan competition for the growing Medicaid population is robust, with several carriers participating and more poised to enter the market for the 2014 Medicaid expansion.

- Trepidation over pricing in the insurance exchange. While most large commercial health plans will participate in the state health insurance exchange for individuals and small businesses, they face considerable uncertainty. Their anxiety stems from the timeline to meet requirements, the potential for adverse selectionŌĆöattracting sicker than average peopleŌĆöin the exchange, and their ability to design products and set premiums while remaining financially viable. In an attempt to mitigate large premium increases in the nongroup market, the state recently took steps to slow the migration of the state’s high-risk pool population to the exchange.

- Medicaid plans’ caution about entering the exchange. A substantial number of people are likely to move between Medicaid and subsidized private coverage as their income fluctuates. If Medicaid plans offer products in the exchange, they may be able to offer more seamless coverage and better continuity of care as people move between the two programs. Nonetheless, Medicaid-only plans are uncertain about entering the exchange because the expertise and growth needed to serve the commercial population could cause financial challenges and detract from providing Medicaid patients with good access to care.

- Broker uncertainty about continued role in the market. Although insurance brokers in the Baltimore region now perform many of the functions needed to assist people buying insurance under reform, their role may shrink because of competition from the exchange and Medicaid outreach organizations seeking to serve as navigators.

Market Background

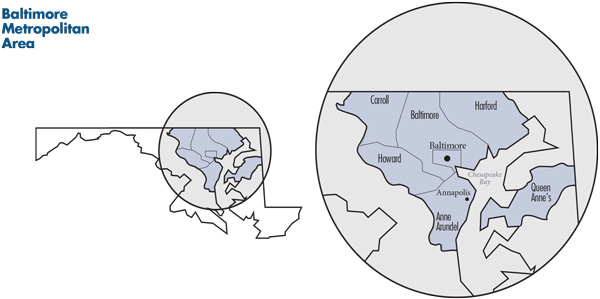

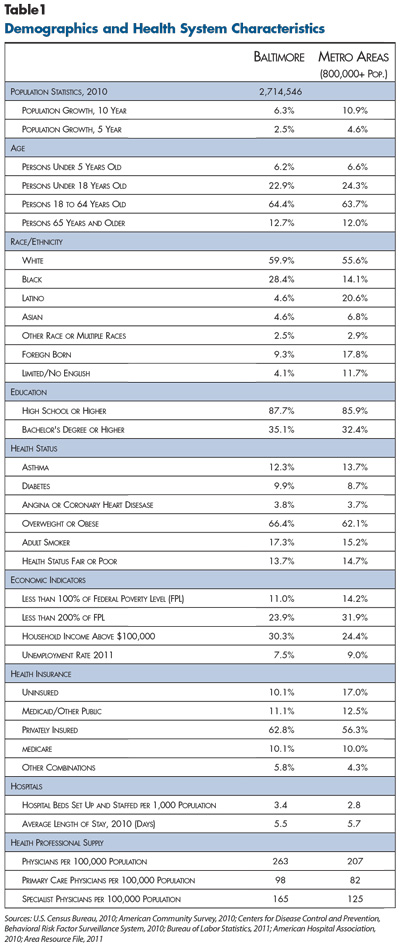

![]() ome to more than 2.7 million people, the Baltimore-Towson metropolitan statistical area encompasses six counties in central and eastern Maryland: Baltimore, Anne Arundel, Carroll, Harford, Howard and Queen Anne’s, plus the city of Baltimore (see map). The region’s overall population has grown more slowly than metropolitan areas on average, with the city of Baltimore’s declining population a key contributing factor (see Table 1).

ome to more than 2.7 million people, the Baltimore-Towson metropolitan statistical area encompasses six counties in central and eastern Maryland: Baltimore, Anne Arundel, Carroll, Harford, Howard and Queen Anne’s, plus the city of Baltimore (see map). The region’s overall population has grown more slowly than metropolitan areas on average, with the city of Baltimore’s declining population a key contributing factor (see Table 1).

The Baltimore metropolitan area spans the extremes of the socioeconomic spectrum from Howard County, one of the highest-income counties in the country, to the city of Baltimore, which has high rates of poverty and poor health.1 Baltimore, a port city, historically was a transportation hub and home to major manufacturers and large national employers. But, many Fortune 500 companies with headquarters in the area left because of broad declines in key industries and a variety of market conditions, including extensive government regulation, high taxes and considerable union presence. Today, the major employers in the Baltimore market include federal, state and local government—and government contractors—public school systems, Johns Hopkins University (including its school of medicine and health system), as well as other hospital systems. Indeed, the area includes Maryland’s capital—Annapolis—and the headquarters of the federal Social Security Administration. Parts of the area also are within commuting distance of downtown Washington, D.C.

A major public-employer presence reportedly has helped buoy the labor market and related health coverage. The region has lower rates of poverty, unemployment and uninsurance, as well as a higher proportion of residents with private health coverage, than other metropolitan areas on average. Still, the recession led to a loss of jobs—unemployment increased from 3.6 percent in 2007 to 7.5 percent in 2011 compared to 9 percent nationally—and related health coverage, with the percentage of private firms offering coverage declining from about 63 percent to 57 percent from 2010 to 2011.2 Overall private insurance coverage declined slightly, from about 65 percent of the population in 2009 to 63 percent by 2011.3

State Embraces Reform

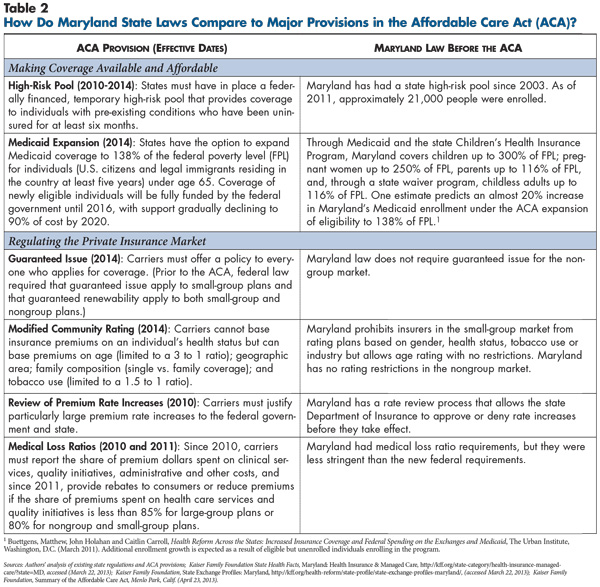

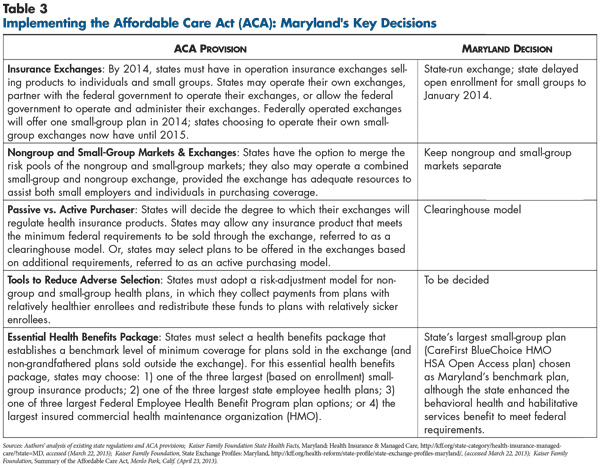

![]() hortly after enactment of national health reform in 2010, Maryland’s Democratic political leaders enthusiastically endorsed the law and began preparing for implementation (see Table 2 and Table 3). With broad support, the Legislature passed the Maryland Health Benefit Exchange Act of 2011 to authorize the state to operate a health insurance exchange—called the Maryland Health Connection. Respondents reported that the state sought broad input from stakeholders to design the exchange, and even respondents highly critical of the ACA reported that the state has acted reasonably in designing the new insurance marketplace for individuals and small businesses.

hortly after enactment of national health reform in 2010, Maryland’s Democratic political leaders enthusiastically endorsed the law and began preparing for implementation (see Table 2 and Table 3). With broad support, the Legislature passed the Maryland Health Benefit Exchange Act of 2011 to authorize the state to operate a health insurance exchange—called the Maryland Health Connection. Respondents reported that the state sought broad input from stakeholders to design the exchange, and even respondents highly critical of the ACA reported that the state has acted reasonably in designing the new insurance marketplace for individuals and small businesses.

Even before passage of national health reform, Maryland pursued changes to commercial insurance regulation, expanded Medicaid and monitored hospital spending through an all-payer rate-setting system.

Commercial insurance regulation. Since the early 1990s, the state has heavily regulated the small-group (2-50 employees) insurance market through modified community rating rules that allow insurers to vary rates based on geography and age but not health status.4 Small-group plans also must meet minimum standards for covered services and limits on patient cost sharing, as established in the state’s Comprehensive Standard Health Benefits Plan (CSHBP). The initial CSHBP, which created a standard product that all small-group carriers must offer and a ceiling on premiums (based on average Maryland wages) was modified in the mid-2000s because it was “too prescriptive and too expensive,” in the words of a broker. To keep premiums below the affordability threshold, the state increased cost-sharing limits. Respondents suggested that the CSHBP currently has little impact on the small-group market because many small employers offer coverage that exceeds the requirements.

In contrast, Maryland has adopted relatively few consumer protections for the individual, or nongroup, insurance market. For example, the state does not require guaranteed issue of coverage, restrict rates or offer subsidies. Other than inclusion of 45 mandated services, insurers need not offer standardized coverage. Maryland’s medical loss ratio standards—which spell out the proportion of premiums that must go toward medical care rather than other expenses—for nongroup insurers are less stringent than the subsequent ACA requirements. The average annual premium for nongroup coverage in Maryland mirrored the national average of approximately $2,600 in 2010.

In 2003, Maryland created a high-risk pool—the Maryland Health Insurance Plan (MHIP)—for people denied commercial coverage based on their health status. Premiums for these products are capped at 150 percent of the average rate, with the state covering excess costs and providing additional subsidies for low-income people. The ACA required all states to offer a temporary high-risk pool program similar to Maryland’s until 2014 and provided federal funding to do so. Maryland grafted the new high-risk pool—MHIP Federal—onto the existing MHIP.

For both individuals and small groups, Baltimore-area brokers typically both sell insurance and perform such administrative functions as eligibility determination and billing—this is known as a “general agent structure.” Health plans work closely with brokers, in what one respondent called a “symbiotic” relationship.

Medicaid. Medicaid enrollment in the Baltimore market increased considerably in recent years as people lost private coverage and the state expanded Medicaid income eligibility to 116 percent of federal poverty for all adult citizens and legal immigrants. Parents and caretakers receive full Medicaid benefits, and childless adults receive a pared-down benefits package through the Primary Adult Care (PAC) program. Between December 2007 and 2009, Maryland Medicaid enrollment grew by a third—from about 537,000 to 715,000 enrollees—compared to 14 percent growth nationally.5 In the Maryland Children’s Health Program—the state’s Children’s Health Insurance Program (CHIP)—income eligibility is 300 percent of poverty, and the program has relatively stable enrollment.

Although state-funded outreach activities to identify potential enrollees ramped up after the Medicaid expansion, current outreach largely is limited to efforts supported by private funding and concentrated in the high-need area of the city of Baltimore and surrounding Baltimore County. The state has streamlined the Medicaid application process somewhat—more so for CHIP. Still, respondents characterized the process as “antiquated,” citing Medicaid requirements for an initial in-person interview by a county agency and mailing completed applications as opposed to faxing or via the Internet. Also, verification systems are not well automated, causing delays in coverage.

With full federal funding for the first three years under the ACA, Maryland plans to expand Medicaid eligibility to 138 percent of poverty—about $14,850 for a single person—in 2014. Childless adults now covered through the PAC program will transition to Medicaid and gain more comprehensive coverageŌĆönamely, coverage for hospitalizations and specialty care. The impact of this expansion on coverage will be relatively small for the Baltimore area compared to communities in other states, many of which cover few childless adults. Still, service utilization in the Medicaid program could spike with the transition because of pent-up demand for services not covered by PAC and by the high medical needs among PAC enrollees.

Providers. Maryland is one of two states with a system that sets the prices of hospital services for all public and private payers (see box below for more about the rate-setting system). Four large hospital systems: Johns Hopkins Medicine, MedStar Health, University of Maryland Medical System (UMD) and LifeBridge Health serve the market. Johns Hopkins clearly stands out based on a national and international reputation as a premier teaching hospital.

The Maryland rate-setting system prevents hospitals from offering private payers discounts to gain patient volume. Instead, hospital strategies to increase volume—common in many markets across the country—include acquiring struggling community hospitals and employing physicians. Employing physicians helps hospitals gain referrals and admissions and increases leverage to negotiate higher payment rates for physicians’ professional services, which are not regulated by the state.

Respondents indicated that people with Medicaid and CHIP coverage have relatively good access to care through an extensive set of hospitals, community health centers, hospital-affiliated primary care physicians (PCPs) and some private physician practices participating in public programs. The rate-setting system removes financial disincentives for hospitals to treat Medicaid patients because hospitals receive approximately the same rate regardless of the patient’s insurance. However, rate setting does not apply to physician services. And, Medicaid payments for physician services are lower than Medicare and private payments, so physicians have less of an incentive to treat Medicaid patients. Still, as of 2008, the Medicaid fee schedule paid PCPs about 80 percent of Medicare rates, which is relatively high among states.8

Hospital Rate Setting in Maryland In 1971, Maryland established the Health Services Cost Review Commission (HSCRC) to set prices for all payers for inpatient and outpatient hospital services. Payment rates are set annually using a formula that takes into account each hospital’s patient population—for example, if the hospital serves many uninsured patients and, therefore, has high uncompensated care costs—and allows for some modification based on hospital efficiency and quality scores. Although rates vary somewhat across hospitals, all payers, including Medicare, Medicaid and private insurers, pay similar rates.6 When Medicare adopted an inpatient prospective payment system for hospitals in 1983, Maryland received a waiver from the Health Care Financing Administration—now the Centers for Medicare and Medicaid Services (CMS)—allowing the state to continue setting rates for Medicare patients. The waiver requires that the rate of growth of Medicare payments per hospital admission in Maryland stay below the national rate, but a 2012 HSCRC report to the governor found that Maryland’s growth rate now approximates the national average. State officials attribute the higher cost growth to such factors as rising uncompensated care costs and movement of services to outpatient settings with remaining patients who are admitted sicker and more expensive. In March 2013, the HSCRC submitted a proposal to CMS for a revised waiver that would limit increases in inpatient and outpatient hospital costs to the rate of growth of the state economy. The proposal also diminishes current hospital incentives to perform more procedures and increases incentives for reducing readmissions and coordinating care among providers.7 |

Comprehensive Employer Coverage

![]() espondents reported that both public and private employers provide relatively comprehensive health coverage in the Baltimore area. While the percentage of large private firms in Maryland offering coverage is on par with the national average, the offer rate among small firms is higher than average, and respondents indicated that offer rates in Baltimore are similar to those of the state overall.9 The average employee contribution in Maryland as a share of the total premium—23 percent for single coverage in 2010—is similar to the national average.10

espondents reported that both public and private employers provide relatively comprehensive health coverage in the Baltimore area. While the percentage of large private firms in Maryland offering coverage is on par with the national average, the offer rate among small firms is higher than average, and respondents indicated that offer rates in Baltimore are similar to those of the state overall.9 The average employee contribution in Maryland as a share of the total premium—23 percent for single coverage in 2010—is similar to the national average.10

Employers in the Baltimore market offer a wide range of health benefits that vary by employer size. Typically, respondents pointed to preferred provider organization (PPO) products as popular in the large-group market, with health maintenance organization (HMO) products more popular among small employers. Large employers reportedly value plans that allow patients to see specialists without a referral, while small groups concerned about costs are more willing to purchase lower-priced HMO products with slightly smaller provider networks and that require referrals for specialist visits.

However, Baltimore-area employers in recent years—like their counterparts in other regions—have increased the share of employee premium contributions and patient cost sharing at the point of service through higher deductibles, coinsurance and copayments. Though some employers reportedly continue to pay the full premium for employees and generously support family coverage, both large and small employers more typically pay 50 percent to 75 percent of individual premiums and 25 percent to 50 percent of family premiums. According to a benefits consultant and broker respectively, $300-$500 is typical for an individual deductible in a large group and $1,200 for someone in a small group.

Respondents noted a lack of innovation in health plan product design, and changes to control costs resemble those found in many other markets. For example, smaller and smaller firms are turning to self-insurance—assuming the financial risk for the cost of enrollees’ care instead of buying insurance—to insulate themselves from the costs associated with Maryland’s strict small-group insurance regulations. Maryland law also allows firms to purchase stop-loss insurance with attachment points as low as $10,000, meaning the stop-loss insurer is responsible once a patient’s claims exceed that amount. Also, while many employers have implemented wellness features—commonly periodic health assessments and, in some cases, participation-based or outcomes-based financial incentives—to encourage healthy behaviors, employee participation reportedly is low.

Employers also face difficulties implementing products with limited-provider networks. Contributing factors include employees’ long-established preference for broad choice of providers; plans’ inability to negotiate discounts—because of the rate-setting systemŌĆö—with hospitals in exchange for volume; and the need for state approval to tier physicians based on performance. A key exception is a limited-network coverage option—Medstar Select Plan—available to Medstar employees that includes only Medstar providers. Medstar employees also have access to a CareFirst PPO built on the Medstar network that increases cost sharing to see providers in an extended network and even greater cost sharing for out-of-network providers.

High-Deductible Health Plans Increase

![]() oth employers and individuals increasingly are choosing high-deductible health plans (HDHPs) with lower premiums. HDHPs, on either a PPO or HMO platform, are growing in prevalence across all employer sizes and in the individual market. Many large employers have started offering HDHPs as an option alongside other, more traditional plans, but employee take up is reportedly low.

oth employers and individuals increasingly are choosing high-deductible health plans (HDHPs) with lower premiums. HDHPs, on either a PPO or HMO platform, are growing in prevalence across all employer sizes and in the individual market. Many large employers have started offering HDHPs as an option alongside other, more traditional plans, but employee take up is reportedly low.

Health plan respondents indicated that less than 20 percent of large-group enrollees are in HDHPs, and only a few large employers have switched to HDHPs as full-replacement products, meaning they only offer HDHPs. Brokers reported considerably higher take up in the small-group market, estimating that about a third of small employers offer only an HDHP. A 2011 state report found even higher take up statewide, with almost half of people in small-group plans enrolled in an HDHP.11

HDHPs in the market commonly are tied to tax-advantaged accounts—either a health savings account (HSA) or health reimbursement account (HRA). The major difference between the two is that HRA balances revert to the employer if the employee leaves. Some large employers reportedly contribute amounts equal to deductibles to HSAs or HRAs, reducing employees’ exposure to high out-of-pocket costs and incentives to make cost-conscious decisions about care. Also, employers have been slow to offer price and quality tools to help employees select higher-value providers, although health plans reportedly are developing such tools.

CareFirst Dominant

![]() he Baltimore-area commercial insurance market has consolidated over the last 25 years. National carriers entered the market primarily through acquisitions of local health plans, which has left the health plan market fairly concentrated. These mergers include Aetna’s purchase of NYLCare (late-1990s to early 2000s), United’s purchase of MAMSI (2004), CIGNA’s purchase of Great West (about 2010), and Aetna’s recent purchase of Coventry (still in process).

he Baltimore-area commercial insurance market has consolidated over the last 25 years. National carriers entered the market primarily through acquisitions of local health plans, which has left the health plan market fairly concentrated. These mergers include Aetna’s purchase of NYLCare (late-1990s to early 2000s), United’s purchase of MAMSI (2004), CIGNA’s purchase of Great West (about 2010), and Aetna’s recent purchase of Coventry (still in process).

Respondents concurred that CareFirst BlueCross BlueShield is the dominant plan overall, with just less than 45 percent of the overall commercial market and 60 percent to 75 percent of the small-group and individual markets. As a regional Blues plan, CareFirst is less popular among large, national self-insured employers. Roughly in order of overall market share, the other major carriers are UnitedHealth Group, Aetna, CIGNA and Kaiser Permanente. United mostly operates in the large-group market but also focuses on the small-group market. CIGNA predominantly operates in the large-group market. After CareFirst, Aetna and Kaiser are reportedly the largest players in the individual market.

Although respondents reported that insurance products are quite similar overall, they also noted that carriers differentiate themselves through certain administrative and product features. For example, United has sophisticated information technology, wellness programs with member incentives and its Premium Designation Program, which ranks physicians in certain specialties based on cost and quality indicators. Members can access provider-specific price information online or through mobile applications on smart phones. United’s Edge product offers lower cost sharing to patients receiving care from physicians rated high performers through the Premium Designation Program. Kaiser is known for its integrated delivery system and CareFirst for its Healthy Blue product, which rewards members for healthy behaviors. CareFirst also has a new patient-centered medical home (PCMH) initiative (see box below for more about the program and other new payment arrangements).

The shrinking pool of commercially insured people has increased pressure on carriers—particularly United, Aetna, CIGNA and Kaiser—to retain or gain enrollment. Health plans try to keep premiums down by managing administrative and marketing expenses, and some respondents noted considerable price competition among plans to gain and keep customers. CareFirst enjoys strong brand-name recognition and loyalty among consumers, and the nonprofit insurer faces regulatory pressure to bring down large reserves. Slower growth in CareFirst rates to bring down reserves affects competitors as well.

Kaiser opened a new facility, the 130,000-square-foot South Baltimore County Corner Medical Center, in April 2013. With 330 physicians and staff, this facility increased Kaiser’s total provider capacity in the market by at least 50 percent, allowing Kaiser to provide some services it previously contracted with others to provide—for example, 24-hour lab, radiology and urgent care. Kaiser also increased the number of physicians in the Permanente Medical Group by about a third, increasing capacity for specialty care. Kaiser will continue to contract with hospitals for inpatient care. Despite these expansions, other health plans did not appear to view Kaiser as a major competitive threat.

Limited New Payment Arrangements The Baltimore market exhibits limited moves toward new payment arrangements among health plans and providers. New arrangements typically involve physicians but not hospitals, reportedly because Maryland hospitals, which are exempt from Medicare’s inpatient prospective payment system, cannot operate Medicare accountable care organizations (ACOs)—a group of providers that agrees to be held accountable for the quality, cost and overall care of a defined group of patients. To date, CMS has approved nine area physician organizations as Medicare ACOs. The broadest new payment arrangement appears to be CareFirst’s patient-centered medical home initiative, which has goals to improve care coordination and decrease overall utilization, especially hospital readmissions and emergency department visits. Implemented in 2011, an estimated 80 percent to 95 percent of primary care physicians in CareFirst’s network participate in the PCMH program, with approximately 2,500 primary care physicians and nurse practitioners in Maryland. Participating providers receive increased fee-for-service rates, plus bonus payments for meeting cost and quality goals. Other payers are interested in single-carrier PCMH models. In February, CIGNA received state approval to offer its nationally recognized PCMH program to a limited number of larger practices.12 United also has signaled interest in launching a single-carrier model. Maryland’s state-sponsored, multi-payer PCMH initiative involves about 350 providers in roughly 50 practices. Under the state program, insurers pay practices to change approaches to care delivery and care management. A shared-savings formula rewards practices that meet quality thresholds and reduce total cost of care for patients attributed to the practice. The state limited participation in the program during the three-year pilot, which ends in July 2014. A larger scale program will be designed based on results from the pilot, and a formal program evaluation is now underway. CMS has awarded Maryland $2.4 million to expand the state PCMH program and foster collaboration with community-based resources to reach more patients, particularly in neighborhoods with the highest levels of chronic health conditions. |

Considerable Plan Competition for Medicaid Enrollees

![]() ith managed care mandatory for all Medicaid enrollees except those dually eligible for Medicaid and Medicare, about 75 percent of Medicaid enrollees take part in the state’s managed care program, HealthChoice. The state allows all plans meeting basic requirements to contract with HealthChoice rather than requiring competitive bidding.

ith managed care mandatory for all Medicaid enrollees except those dually eligible for Medicaid and Medicare, about 75 percent of Medicaid enrollees take part in the state’s managed care program, HealthChoice. The state allows all plans meeting basic requirements to contract with HealthChoice rather than requiring competitive bidding.

Seven health plans serve Baltimore-area Medicaid enrollees, with none dominant. Two national for-profit plans—Amerigroup (now part of WellPoint) and United—have large market shares (about 25% and 18%, respectively), and Coventry entered the market about three years ago and remains a smaller player. The remaining plans are provider owned, including Priority Partners (owned by Johns Hopkins and a group of community health centers), also with about a 25-percent market share, followed by provider-owned Maryland Physicians Care. MedStar Family Choice and Jai Medical Systems, a physician-owned plan limited to the city of Baltimore, are smaller. Plans participating in Medicaid also must participate in CHIP and hold similar shares of that market. Amerigroup, United, Jai Medical Services and Priority Partners also participate in the PAC program, the scaled-down program for childless adults.

While Medicaid health plans’ enrollment increased significantly after the Medicaid expansion, market shares among Medicaid plans have been relatively stable in recent years but vary somewhat by geography. For example, Priority Partners has a larger share on the east side of the city of Baltimore because of the location of Johns Hopkins facilities.

The main way Medicaid plans differentiate themselves from competitors is through additional covered services—primarily dental care because the state no longer covers this service for adults. Some plans had dropped dental care for cost reasons but found they had to add it back to stay competitive. Also, since 2003, the state has issued annual quality report cards to help enrollees select a plan and to assign enrollees to plans if they do not select one themselves. Local plans perform better than the national plans. As one plan respondent said, “State policy drove us into [quality measurement] activities faster than we would have otherwise.” Also, accreditation by the National Committee for Quality Assurance is gaining importance among plans and the state. Despite these efforts, a respondent involved in outreach considers the plans pretty similar overall.

After the state’s Medicaid expansion, some Medicaid plans’ per-member costs increased as new enrollees used more services than existing enrollees, leading to significant financial losses for some plans. Respondents attributed this spike to pent-up demand from previously uninsured enrollees. According to one plan respondent, new enrollees were “accessing health care in unprecedented ways.” For example, in the first year after the expansion, one plan faced a significant increase in organ transplants—from one to five.

Over time, however, the Medicaid plans typically found that most new enrollees had similar health status or were healthier than existing Medicaid enrollees, and plans’ utilization and financial positions largely stabilized or improved. As one plan respondent recalled, “The good news is that we got through that, but it took about six months from date of enrollment before people settled down [with their utilization] a bit.”

Additionally, Medicaid health plans had to adjust to state premium reductions (about 10% across the board) over the last 3-4 years. Unlike states without hospital rate setting, Medicaid plans in Maryland cannot reduce hospital payments when their state payments are cut.

Still, payments to plans are adjusted annually based on geography and enrollee health status. Some plan executives reported that this risk-adjustment process initially was collaborative and based on actual encounter data, but the process has become less transparent. The result, according to one respondent, is that now “rates are just handed to plans.” When Medicaid expanded, some plans reportedly were savvier in attracting lower-risk enrollees and limiting exposure to higher-risk ones, particularly by adjusting the location and types of providers in plan networks.

Additional health plans are interested in serving the Baltimore-area Medicaid population. These reportedly include Medicaid-only plans, including Riverside Health and Molina, as well as some commercial plans. Kaiser plans to enter the Medicaid market in fall 2013, Aetna holds the management agreement for Maryland Physicians Care and has bought Coventry, and WellPoint bought Amerigroup. Additionally, some respondents reported that national plans are interested in purchasing local provider-owned Medicaid plans.

Reform Preparations

![]() cross the country, open enrollment in health insurance exchanges is slated to begin Oct. 1, with the Medicaid expansion following on Jan. 1, 2014. The Baltimore area appears more prepared than most markets, although the state, health plans and others still have much work to do. While many respondents supported health reform goals, they had considerable concern about meeting deadlines and the eventual impact on health coverage.

cross the country, open enrollment in health insurance exchanges is slated to begin Oct. 1, with the Medicaid expansion following on Jan. 1, 2014. The Baltimore area appears more prepared than most markets, although the state, health plans and others still have much work to do. While many respondents supported health reform goals, they had considerable concern about meeting deadlines and the eventual impact on health coverage.

The Maryland insurance exchange will follow a clearinghouse model, meaning any insurer meeting minimum federal requirements will be permitted to offer products. Maryland requires that all but the smallest nongroup and small-group insurers participate. The exchange will maintain separate risk pools for the small-group and individual markets. Maryland’s exchange will be funded by an existing 2 percent tax on health insurers. While open enrollment in Maryland’s individual exchange is slated to begin Oct. 1, the state has delayed open enrollment for small groups until January 2014.

Uncertainties in Setting Premiums in the Exchange

![]() cross the country, there are likely to be similar questions and concerns about setting premiums for products offered in the exchanges, including:

cross the country, there are likely to be similar questions and concerns about setting premiums for products offered in the exchanges, including:

- Risk pools—how sick will the newly insured be compared to the already insured? Will young and healthy enrollees drop out because of higher rates and instead pay the tax penalty? Which small groups will drop coverage and how will this affect the risk pool?

- Pent-up demand—will the newly insured make up for months and years of forgone care by using large amounts of medical care?

- Expanded benefits—how much utilization will occur, and how much will premiums increase because ACA minimums exceed benefits of many existing plans, especially in the nongroup market?

- Risk adjustment—how will the health status of enrollees be measured, and how will funds be redistributed among carriers? Will this process adequately account for differences in risk profiles of plan members?

Along with these broader concerns, there are some ways these issues could play out more specifically in the Baltimore market.

Actuarial anxiety. Across markets, commercial health plans face the challenge of setting premiums for exchange products. When setting premiums, plans rely on actuaries’ projections of medical claims. Typically, the pool of enrollees and plan design are fairly stable from one year to the next, with underlying provider cost trends being the only major source of uncertainty—being off by one or two percentage points is viewed as a major error. Reform presents additional uncertainty, largely related to how sick the newly insured population will be and how many health services people will use.

Compounding the actuarial anxiety is the perception that setting premiums is a no-win proposition. If premiums are set too high, the new minimum medical loss ratio requires excess premiums to be returned to policyholders. But, if premiums are set too low, plans will lose money and the state’s annual rate review process could prevent plans from raising future premiums sufficiently. One Baltimore health plan executive summed it up as, “So what is a small opportunity [to add new business] could really wreak havoc.”

Maryland selected one of the largest small-group plans in the state, a CareFirst HMO, to be its essential health benefits benchmark plan.┬ĀThis product has a slightly lower cost and narrower scope of benefits relative to some of the other possible benchmark options, though the state has made some enhancements to the plan.

Health plan executives expect large overall premium increases—particularly for young, healthy individuals—in the nongroup market during the transition from an essentially unregulated market to one with essential health benefits requirements and modified community rating rules. They also noted concern about the cost effect of rolling the more than 20,000 people in Maryland’s high-risk pool into the broader nongroup pool. However, for some consumers with pre-existing conditions, modified community rating rules may result in lower premiums, since insurers will not be able to vary premiums based on health status.

Despite existing tight regulation of the small-group market, some respondents predicted “rate shock” for small employers. If rates do increase sharply, it may prompt small employers to adopt defined contributions for their employees to purchase coverage in the exchange or to stop offering coverage, according to respondents.

Threats to CareFirst’s dominance. The insurance exchange may provide an opportunity for health plans to gain market share, potentially threatening CareFirst’s dominance in the nongroup and small-group markets. CareFirst’s reputation and name recognition may become less important because exchange products are expected to be standardized on the basis of actuarial value and easier to compare on a head-to-head basis of “price, price and price,” as one respondent characterized the new competitive field. However, if sicker people gravitate to CareFirst, the insurer could face significant cost increases. Moreover, some respondents expect other carriers to experiment with product design to differentiate themselves in the exchange. And, CareFirst’s close relationship with brokers—reportedly CareFirst pays higher commissions—may be less helpful if the new exchange bypasses brokers and links carriers directly with customers.

A new competitive arena for plans. The deep historical divide between commercial and Medicaid insurers in many markets is expected to narrow under reform. Even for carriers, such as United, that offer both commercial and Medicaid products, these products typically function as separate business lines, operating under different rules and using different provider networks. While no Medicaid-only plans will participate in the exchange initially, both types of plans may mingle in the Maryland insurance exchange in the future.

Respondents cited some competitive advantages that commercial plans hold over Medicaid plans. Commercial carriers, especially national ones, can easily satisfy the exchange’s capital-reserve requirements and fund intense marketing campaigns to alert people about new coverage options. Also, commercial plans tend to have broader provider networks than provider-owned Medicaid plans.

Another change to the competitive dynamics on the exchange will be the entry of a new health plan, a member-run, nonprofit co-op plan called Evergreen Health Cooperative. In addition to a more traditional insurance product, Evergreen initially will offer a plan with a patient-centered medical home structure for residents of Baltimore. Doctors participating in this plan will be salaried, and one analysis predicted that the premiums for this product will be 20 percent to 30 percent less than products offered by major commercial carriers.13

At the same time, respondents noted considerable state pressure for Medicaid health plans to enter the exchange and offer commercial products. This could help improve coverage continuity and mitigate the churning of people between Medicaid and subsidized private coverage because of income fluctuations. Indeed, Medicaid plans also would have some advantages if they do participate in the exchange. Compared to commercial insurers, Medicaid plans are growing, and the plans are more experienced than commercial carriers in meeting the needs of lower-income people. Likewise, Medicaid plans are experienced in controlling costs under fixed—and recently declining—payment rates.

Yet, Medicaid-only plan executives had mixed levels of interest in entering the private insurance arena. Some expressed concern about growth negatively affecting their mission to prioritize access to services for the lowest-income individuals and/or their financial bottom line. Indeed, they are already bracing for the same pent-up demand experienced after the state’s Medicaid expansion a few years ago and are concerned about the financial impact, even if temporary. As one plan respondent predicted, “At the beginning of 2014, we will get slammed again.”

Varied predictions for brokers. The goal of streamlining shopping for health insurance by connecting buyers and sellers directly through an insurance exchange puts the role of Baltimore-area insurance brokers in question. The ACA’s minimum loss ratio places more pressure on brokers because their commissions count toward health plans’ administrative expenses. Local brokers fear their core business model is in jeopardy, and some are diversifying into other insurance lines, such as automobile and property coverage.

On the other hand, some respondents suggested that the current general agent structure gives brokers and the market a leg up on reform, as brokers already possess many of the capabilities needed to work with the insurance exchange and help people navigate coverage options. Maryland, unlike some other states, is not barring brokers from selling exchange plans. One broker pointed out that the ACA’s complexities have heightened the need for brokers among small employers without human resource departments and expertise in securing employee health benefits. However, the state has funded three nonprofit organizations to serve as navigators to help small employers and individuals to enroll in private or public coverage.

Given Maryland’s previous Medicaid expansion, outreach efforts will not face as “deep a dive,” as one respondent said, to identify and help people apply for Medicaid or other coverage as in some other parts of the country. Still, the state is working to improve information technology systems to improve the enrollment process. Overall, respondents believed plan and provider capacity will be relatively good to meet the needs of an expanded Medicaid population.

Issues to Track

![]() s health reform unfolds in the coming years, there will be ongoing issues to track in the Baltimore-area health care market, including:

s health reform unfolds in the coming years, there will be ongoing issues to track in the Baltimore-area health care market, including:

- How will Maryland’s hospital rate-setting system change under a new federal waiver? Will it push providers and plans to pursue ACO and bundled payment contracting?

- How will insurance products change as payers seek ways to hold down premium increases? Will the market continue to see more take up of high-deductible health plans? Will limited-network products gain traction?

- What impact will patient-centered medical homes have on care delivery? Will other new payment models, such as ACOs, gain ground in the market, regardless of changes in the rate-setting system?

- To what extent will pent-up demand from newly covered people occur, and will there be sufficient provider capacity to meet those needs?

- How will premiums change in the small-group and individual insurance markets? Will “rate shock” discourage people from enrolling?

- Will more small employers start self-insuring workers’ health benefits to avoid new regulations under reform? What effect would increased self-insurance have on rates in the fully insured market?

- How will the role of insurance brokers change, and what impact will there be on how employers and individuals shop for health insurance?

- How will Medicaid health plans fare under reform? To what extent will they participate in the exchange? Will national plans prove successful in acquiring provider-owned Medicaid plans?

Notes

| 1. | Robert Wood Johnson Foundation, County Health Rankings & Roadmaps, http://www.countyhealthrankings.org/ (accessed March 22, 2013). |

| 2. | Agency for Healthcare Research and Quality, Center for Financing, Access and Cost Trends, Medical Expenditure Panel Survey-Insurance Component, Table IX.A.1(2011), Health Insurance Offer, Eligibility and Take Up Rates for Private-Sector Establishments and Employers for Areas within States, United States 2011, http://meps.ahrq.gov/mepsweb/data_stats/summ_tables/insr/state/series_9/2011/tixa1.htm (accessed March 22, 2013). |

| 3. | U.S. Census Bureau, American Community Survey, 2009 and 2011. |

| 4. | Maryland Health Care Commission, Maryland’s Small Group Health Insurance Market: Summary of Carrier Experience for the Calendar Year Ended December 31, 2001, Baltimore, Md. (June 21, 2002). |

| 5. | Kaiser Commission on Medicaid and the Uninsured, Medicaid Enrollment: December 2009 Data Snapshot, Washington, D.C. (September 2010). |

| 6. | Sommers, Anna S., Chapin White and Paul B. Ginsburg, Addressing Hospital Pricing Leverage through Regulation: State Rate Setting, Policy Analysis No. 9, National Institute for Health Care Reform, Washington, D.C. (May 2012). |

| 7. | Maryland Department of Health and Mental Hygiene, Maryland’s Model Design: Model Design Proposal to the Center for Medicare and Medicaid Innovation, Baltimore, Md. (March 26, 2013). |

| 8. | Kaiser Family Foundation, State Health Facts, Medicaid-to-Medicare Fee Index, 2012, http://www.statehealthfacts.org/comparetable.jsp?ind=196&cat=4 (accessed March 22, 2013). |

| 9. | Agency for Healthcare Research and Quality, Center for Financing, Access and Cost Trends, Medical Expenditure Panel Survey, Insurance Component, Table II.A.2(2011), Percent of Private-Sector Establishments that Offer Health Insurance by Firm Size and State, United States 2011, http://meps.ahrq.gov/mepsweb/data_stats/summ_tables/insr/state/series_2/2011/tiia2.htm (accessed March 22, 2013). |

| 10. | Maryland Health Care Commission, Medical Expenditure Panel Survey Insurance Component: Maryland Sample Through 2010, Baltimore, Md. (January 2012). |

| 11. | Maryland Health Care Commission, Maryland’s Small Group Health Insurance Market: Summary of Carrier Experience for the Year Ending December 31, 2011, Baltimore, Md. (June 21, 2012). |

| 12. | Larson, Bridget K., et al., “Insights From Transformations Under Way at Four Brookings-Dartmouth Accountable Care Organization Pilot Sites,” Health Affairs, Vol. 31, No. 11 (November 2012). |

| 13. | James, Julia, “Health Policy Brief: The CO-OP Health Insurance Program,” Health Affairs (Feb. 28, 2013). |

Data Source

As part of the Robert Wood Johnson Foundation’s (RWJF) State Health Reform Assistance Network initiative, the Center for Studying Health System Change (HSC) examined commercial and Medicaid health insurance markets in eight U.S. metropolitan areas: Baltimore; Portland, Ore.; Denver; Long Island, N.Y.; Minneapolis/St. Paul; Birmingham, Ala.; Richmond, Va.; and Albuquerque, N.M. The study examined both how these markets function currently and are changing over time, especially in preparation for national health reform as outlined under the Patient Protection and Affordable Care Act of 2010. In particular, the study included a focus on the impact of state regulation on insurance markets, commercial health plans’ market positions and product designs, factors contributing to employers’ and other purchasers’ decisions about health insurance, and Medicaid/state Childrens’ Health Insurance Program (CHIP) outreach/enrollment strategies and managed care. The study also provides early insights on the impact of new insurance regulations, plan participation in health insurance exchanges, and potential changes in the types, levels and costs of insurance coverage.

This primarily qualitative study consisted of interviews with commercial health plan executives, brokers and benefits consultants, Medicaid health plan executives, Medicaid/CHIP outreach organizations, and other respondents—for example, academics and consultants—with a vantage perspective of the commercial or Medicaid market. Researchers conducted 19 interviews in the Baltimore market between September 2012 and January 2013. Additionally, the study incorporated quantitative data to illustrate how the Baltimore market compares to the other study markets and the nation. In addition to a Community Report on each of the eight markets, key findings from the eight sites will also be analyzed in two publications, one on commercial insurance markets and the other on Medicaid managed care.