Health Care Market Stabilizes, but Rising Costs and State Budget Woes Loom in Boston

Community Report No. 12

Fall 2003

John F. Hoadley, Debra A. Draper, Sylvia Kuo, Peter J. Cunningham, Jessica Mittler, Len M. Nichols, Gloria J. Bazzoli, Justin White, Robert A. Berenson

In May 2003, a team of researchers visited Boston to study that community’s health system, how it is changing and the effects of those changes on consumers. The Center for Studying Health System Change (HSC), as part of the Community Tracking Study, interviewed more than 90 leaders in the health care market. Boston is one of 12 communities tracked by HSC every two years through site visits and every three years through surveys. Individual community reports are published for each round of site visits. The first three site visits to Boston, in 1997, 1999 and 2001, provided baseline and initial trend information against which changes are tracked. The Boston market includes the city of Boston and Bristol, Essex, Middlesex, Norfolk, Plymouth and Suffolk counties.

![]() he Boston health care market has stabilized somewhat after hospital and health

plan contract disputes and financial woes disrupted the market two years ago.

Hospitals’ finances have improved to some extent, but some hospitals continue

to struggle with capacity constraints. Health plans also have recovered financially.

Employers, however, have faced annual double-digit premium increases, leading

many to shift more costs to workers and seek new strategies to slow rising health

care costs. Severe state budget problems prompted some health program cuts,

but the state managed to roll back a major Medicaid eligibility cut and forestall

reductions to the state uncompensated care pool, which threatened to reduce

access and further strain providers, health plans and employers.

he Boston health care market has stabilized somewhat after hospital and health

plan contract disputes and financial woes disrupted the market two years ago.

Hospitals’ finances have improved to some extent, but some hospitals continue

to struggle with capacity constraints. Health plans also have recovered financially.

Employers, however, have faced annual double-digit premium increases, leading

many to shift more costs to workers and seek new strategies to slow rising health

care costs. Severe state budget problems prompted some health program cuts,

but the state managed to roll back a major Medicaid eligibility cut and forestall

reductions to the state uncompensated care pool, which threatened to reduce

access and further strain providers, health plans and employers.

Other important developments include:

- The ongoing budget problems that threaten the state’s movement toward universal health insurance and the viability of the uncompensated care pool.

- The increasing problem of recruiting and retaining physicians and other skilled health care professionals.

- The continuing focus on quality improvement by health plans and providers, putting Boston in the vanguard relative to many other markets.

- Hospital Finances Improve

- Hospital Capacity Constraints

- Physician Recruitment Problems

- Employers and Health Plans Eye Benefit Design Changes

- Boston Hospitals Leap Ahead on Patient Safety, Quality Improvement

- Budget Pressures Threaten Universal Health Care Push

- Issues to Track

- Boston Consumers’ Access to Care, 2001

Hospital Finances Improve

Over the last two years, hospitals’ financial conditions have improved somewhat, with volume up at the major Boston hospitals. Partners HealthCare System, which has the largest market share and includes Massachusetts General and Brigham and Women’s hospitals, reported the best financial results in 2002 since its formation in 1994. Caritas Christi, a Catholic community-based system with the second-largest market share in the Boston area, generally has been stable financially, although its six hospitals continue to operate close to the margin.

At the same time, CareGroup, a system headed by flagship Beth Israel Deaconess Medical Center, dissolved, as did Tufts-New England Medical Center’s relationship with its Rhode Island-based parent, Lifespan. CareGroup, originally a merger of Beth Israel and New England Deaconess hospitals with five community hospitals, exists only as a bond covenant among three of the hospitals. One of the community hospitals, Waltham Hospital, closed in July 2003; another, Deaconess-Nashoba, was sold to a for-profit hospital system; while a third, Deaconess-Glover, merged with the flagship. Meanwhile, under new leadership, Beth Israel Deaconess has improved its financial position and reduced its nursing vacancy rate from double digits to roughly 7 percent. In addition, the hospital continues to streamline operations and eliminate duplicative services resulting from the original merger of Beth Israel and Deaconess.

Community leaders also were anticipating a new round of contract negotiations between Partners and Tufts Health Plan, which were ongoing in fall 2003 and were slated to be followed by Partners’ negotiations with Harvard Pilgrim and Blue Cross Blue Shield of Massachusetts (BCBS). Sensitive to community concerns that its status as a "must-have" provider network could lead to sharp rate increases, Partners was positioning itself carefully for the negotiations, seeking to demonstrate that requested rate increases are reasonable. One strategy is to detail the extent to which the rate increase is dedicated to offsetting the impact of reduced state and federal reimbursements. Partners also has circulated analyses to counter what it considers to be widely held misperceptions about high hospital costs in the Boston market generally and at Partners in particular. Other providers expect to benefit from whatever rate increase Partners obtains, predicting the pacts will set a market pattern.

Hospital Capacity Constraints

![]() ospital emergency department diversions-a major issue two

years ago-have eased somewhat. Still, urban teaching hospitals report bed-occupancy

rates ranging from 85 percent to 100 percent, while community hospitals generally

operate at about 60 percent capacity. The exception is the Caritas Christi system,

whose suburban hospitals reportedly are full and whose urban hospitals are busy.

Overall, many observers have attributed capacity constraints to the number of

hospital closures over the past decade, arguing that the market may have overadjusted

to declining rates of use and pressure on prices in the mid-1990s. Observers

said the shortage of certain health care personnel, including nurses, pharmacists

and laboratory technicians, is another contributing factor. Many also suggested

that consumer preferences for using academic medical centers for care has led

to a concentration of patients in a small number of facilities.

ospital emergency department diversions-a major issue two

years ago-have eased somewhat. Still, urban teaching hospitals report bed-occupancy

rates ranging from 85 percent to 100 percent, while community hospitals generally

operate at about 60 percent capacity. The exception is the Caritas Christi system,

whose suburban hospitals reportedly are full and whose urban hospitals are busy.

Overall, many observers have attributed capacity constraints to the number of

hospital closures over the past decade, arguing that the market may have overadjusted

to declining rates of use and pressure on prices in the mid-1990s. Observers

said the shortage of certain health care personnel, including nurses, pharmacists

and laboratory technicians, is another contributing factor. Many also suggested

that consumer preferences for using academic medical centers for care has led

to a concentration of patients in a small number of facilities.

The Boston market has experienced capacity constraints for long enough that most systems are working actively on solutions, some of which are showing results. Partners is trying to make better use of its capacity and reduce costs by shifting patients from its crowded academic medical centers, Massachusetts General and Brigham and Women’s hospitals, to affiliated community hospitals. One successful step was the merger of Faulkner Hospital with Brigham and Women’s. By moving some services and physicians from Brigham to Faulkner, Faulkner increased its occupancy from a range of 50-60 percent to 80-90 percent.

Several area academic medical centers are moving patients through their institutions

more efficiently. Moving a patient more quickly from the intensive care unit

(ICU) to a regular bed can allow another patient to move from the emergency

department to the ICU, thus relieving pressure on the emergency department.

Physician Recruitment Problems

![]() oston is experiencing problems in physician recruitment and retention, a major change in a market traditionally considered to have an oversupply of physicians. Market observers pointed to the area’s high cost of living, low salaries relative to other parts of the country and high malpractice insurance premiums as leading to problems recruiting physicians from outside the Boston area and retaining physicians who are completing their residency training. Observers also noted that estimates of Boston’s physician supply may be overstated because of the large number of physician researchers at academic institutions who practice only on a limited basis. The most severe shortages were reported in anesthesiology, radiology, gastroenterology and emergency medicine. Growing shortages also were reported for obstetrics/gynecology, neurosurgery, orthopedics, cardiology and general surgery. As a result, patients face much longer appointment waiting times.

oston is experiencing problems in physician recruitment and retention, a major change in a market traditionally considered to have an oversupply of physicians. Market observers pointed to the area’s high cost of living, low salaries relative to other parts of the country and high malpractice insurance premiums as leading to problems recruiting physicians from outside the Boston area and retaining physicians who are completing their residency training. Observers also noted that estimates of Boston’s physician supply may be overstated because of the large number of physician researchers at academic institutions who practice only on a limited basis. The most severe shortages were reported in anesthesiology, radiology, gastroenterology and emergency medicine. Growing shortages also were reported for obstetrics/gynecology, neurosurgery, orthopedics, cardiology and general surgery. As a result, patients face much longer appointment waiting times.

Health plans, however, did not report network disruptions as a result of physician capacity constraints. One exception has been in plans participating in Medicare+Choice, where considerable network disruption has resulted from physicians’ and hospitals’ unwillingness to participate because of low payment rates. Plan respondents said low government payment rates are to blame, resulting in plans pulling back from this line of business.

Employers and Health Plans Eye Benefit Design Changes

Boston employers traditionally have provided generous health benefits, but recent premium increases have captured their attention. Employers fear the current rate of premium increases is unsustainable and are now searching actively for cost-control options. Health plans, in response, are developing a range of new product offerings.

Both health plans and employers are focusing on products with higher patient cost sharing, primarily higher deductibles and copayments to encourage consumers to choose lower-cost options. Observers pointed to the high rate at which patients seek care for routine conditions, such as normal birth deliveries, in expensive academic medical centers rather than in community hospitals. Both BCBS and Tufts Health Plan have introduced tiered-network products where a higher copayment is charged for care at an academic medical center. In addition, two employer coalitions hired Patient Choice Healthcare, Inc., a Minnesota-based firm, to study the feasibility of developing tiered networks for the Boston market. Although Patient Choice concluded tiers were feasible and began to develop networks, Partners declined to participate, citing a number of concerns, including the adequacy of payment rates. Employers are skeptical that tiered networks will succeed in Boston without the inclusion of Partners. Brokers for small employers reported they eagerly sought but could not find tiered-network products, so the extent to which these are being marketed also may be limited.

Despite the high health maintenance organization (HMO) penetration in Boston, some large employers headquartered outside the market are moving to preferred provider organization (PPO) options for locally based employees. In addition, health plans have introduced high-deductible products, some on an HMO platform. BCBS and Harvard Pilgrim have HMO products with an annual deductible for single coverage ranging from $1,000 to $5,000, and Tufts has a new affiliation with Destiny Health for a high-deductible consumer-directed product on a PPO platform.

Health plans also are looking to control costs through new provider payment arrangements, as Boston’s emphasis on risk-based provider payments has increasingly fallen out of favor. Today, providers and health plans are actively moving toward fee-for-service arrangements with a pay-for-performance component that includes incentives for meeting cost and quality targets.

BCBS provides financial incentives to primary care physicians who meet a variety of performance-based indicators for satisfaction and access, such as rates for mammography, retinal screenings and first-line antibiotic use. It recently implemented a similar program for large multispecialty group practices.

Additionally, as hospital contracts come up for renewal, BCBS is building in a quality component so hospitals can receive additional payment beyond their contracted rates if related goals are achieved. Currently, about a third of the hospitals in the network have a quality component in their contracts.

Several large employers in the market are participating in Bridges to Excellence, a pay-for-performance initiative that rewards providers for meeting performance measures believed to improve care. Employers will pay for the incentives while the National Committee for Quality Assurance (NQCA) will identify which physicians qualify for financial awards after evaluating and verifying physician data. An innovative aspect of this initiative is a strong push for physicians to adopt electronic information systems, not just meet outcomes measures. Consumer involvement in Bridges to Excellence is supported by education and a reward system.

In the insurance market, BCBS has emerged as the clear enrollment leader, gaining considerable membership in the last two years-often at the expense of major rivals Tufts Health Plan and Harvard Pilgrim. BCBS is focusing on improving customer service, and the national Blue Card program has contributed to the plan’s membership growth by attracting large, multiple-location employers.

Tufts Health Plan has new leadership and is focusing on a new Web-based information system to increase administrative flexibility and cost efficiency. Harvard Pilgrim, which operated under state receivership for a time, is now financially healthier and once again growing membership. A new executive management team, more aggressive underwriting and shedding of unprofitable business were all factors in the plan’s financial turnaround.

Boston Hospital Leap Ahead on Patient Safety, Quality Improvement

![]() ospitals have made substantial progress in patient safety and quality

improvement in the Boston market, which is not surprising since the area has

been the home of many patient safety innovations. The Leapfrog Group-composed

of more than 140 employers-focuses on three practices it asserts have tremendous

potential to reduce preventable errors: use of computer physician order entry

(CPOE) for prescriptions, evidence-based hospital referrals that rely on volume

standards for certain high-risk procedures and staffing ICUs with intensivists

specially trained to care for critically ill patients.

ospitals have made substantial progress in patient safety and quality

improvement in the Boston market, which is not surprising since the area has

been the home of many patient safety innovations. The Leapfrog Group-composed

of more than 140 employers-focuses on three practices it asserts have tremendous

potential to reduce preventable errors: use of computer physician order entry

(CPOE) for prescriptions, evidence-based hospital referrals that rely on volume

standards for certain high-risk procedures and staffing ICUs with intensivists

specially trained to care for critically ill patients.

Partners’ flagship hospitals, Massachusetts General and Brigham and Women’s, are two of the seven hospitals nationally that fulfill all of Leapfrog’s requirements. The other three Boston academic medical centers also have made substantial headway toward Leapfrog’s goals. For example, Beth Israel Deaconess, one of the first hospitals to substantially comply with Leapfrog, meets the CPOE standard, exceeds the intensivist standard by having them in-house at all times and is just short of fulfilling the volume standard. Boston Medical Center reports 99 percent progress toward CPOE implementation.The hospital also reports full implementation of the intensivist standard, though not in complete compliance with Leapfrog since the intensivists are not completely dedicated to the ICU. Despite the accomplishments, however, some smaller community hospitals in Boston that are challenged by a lack of resources find it difficult to comply with Leapfrog standards.

Other health systems are involved in different patient safety and quality initiatives. Partners is investing in information technology, including electronic medical records and computerization efforts similar to CPOE. It is also working to assure comparable quality across all of the Partners’ hospitals. Caritas Christi has broader quality initiatives, such as risk management and efforts to improve medication labeling. On the plan side, Harvard Pilgrim awards competitive grants of $50,000 to $250,000 to physician practices to develop quality improvement programs. In addition, NCQA recognizes four plans in the Boston market-BCBS, Tufts, Harvard Pilgrim and Fallon-among the top 10 health plans nationally based on Health Plan Employer Data and Information Set (HEDIS) performance standards.

Budget Pressures Threaten Universal Health Care Push

As state and local officials grappled with growing budget deficits, advocates for the poor and safety net providers were concerned that the push in Massachusetts toward universal health care would lose ground. MassHealth, the expanded Medicaid and State Children’s Health Insurance Program that has seen enrollment grow 50 percent since its creation in 1997, recently underwent numerous cutbacks, some of which were subsequently restored. Most notable, eligibility for 36,000 MassHealth Basic beneficiaries-generally chronically unemployed adults, many of whom are substance abusers-was eliminated in April 2003 but reinstated effective October 2003. In restoring eligibility, however, the state capped enrollment in this program at 36,000 and will end it next year unless funding is found. The final state budget included across-the-board 3 percent to 5 percent provider payment rate reductions, elimination of adult dental services and a variety of other cuts. Overall, Medicaid expenditure growth is now projected to be about 9 percent for fiscal year 2004, down from 14 percent before cuts were made.

A key component of Massachusetts’ efforts to provide access for the uninsured is the state uncompensated care pool, which subsidizes the cost of providing care to the uninsured at hospitals and community health centers. The pool faces significant financial pressures because of public program cuts and increasing numbers of uninsured people.

Distribution and accountability of funds from the uncompensated pool also have caused controversy. Entering the budget debate, core funding came from a hospital assessment, a surcharge on private insurers and state funding. Revenue sources are set by law, so unless the state Legislature makes up the shortfall by finding additional funds or increasing contributions of hospitals and/or insurers, the pool is unable to pay hospitals the full cost of their uncompensated care.

The two safety net hospitals in the community, Boston Medical Center and Cambridge Health Alliance, provide by far the largest amount of uncompensated care and thus are the primary pool recipients. Smaller community hospitals, many of which are struggling financially, resent paying into the pool when they see surpluses at some safety net hospitals that draw large sums from the pool.

The Legislature and the various interests fought considerably during this year’s budget debates over how to pay for the pool and address accountability issues, generating significant crossfire among providers and accentuating divisions among hospitals in the state. In the end, the Legislature resolved the pool’s funding with a mix of new federal dollars-a one-time increase from federal tax cut legislation, an increased health plan surcharge and several other revenue sources. However, the state is capping payments to both hospitals and community health centers at roughly last year’s levels and is considering additional changes to the pool that would shift funding from Boston Medical Center and Cambridge Health Alliance to other hospitals.

Despite the recent budget tumult, the financial health of Boston’s safety net providers appears to be about the same as it was two years ago. Boston has traditionally had a strong safety net, anchored by Boston Medical Center and Cambridge Health Alliance and bolstered by an unusually strong network of community health centers and a well-established tradition of caring for the uninsured. As of mid-2003, the large safety net hospitals were in modestly better shape, and community health centers probably a bit worse off, than two years ago. Safety net hospitals ran surpluses in the most recent fiscal year, thanks to payments from the free-care pool and management improvements, but they project losses for the current year and beyond because of increases in the number of uninsured patients.

Community health centers are starting to see the effects of reduced funding but have dealt with it by tightening management and jettisoning programs not directly relevant to providing services. Some centers have managed to expand, mostly by using federal dollars received through federal expansion and community access program grants or funds from affiliated hospitals. Looking to the future, safety net providers are worried that rising numbers of uninsured people and zero growth in financial support will weaken their position in the next few years.

Issues to Track

Ongoing budget pressures continue to expose the vulnerability of public programs and the financial stability of providers delivering care to the uninsured. At the same time, health plans and employers are grappling with the rising cost of health care and exploring new product innovations with increased patient cost sharing as a potential solution.

Key issues to track include:

- To what extent will state budget shortfalls result in public program cuts, or will policy makers continue to forge compromises to avoid severe cuts?

- How will ongoing issues concerning the uncompensated care pool be addressed?

- Will academic medical centers solve current capacity constraints by finding more ways to shift patients to community hospitals, or will the overall trend toward rising utilization slow, thereby reducing pressure to use capacity more efficiently?

- Will physician recruitment and retention difficulties evolve into physician shortages?

- Will new health benefit design innovations take hold in Boston and help to moderate rising health care costs?

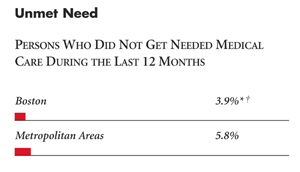

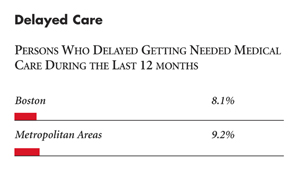

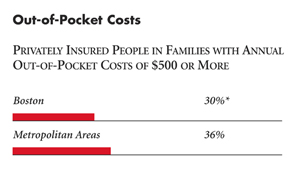

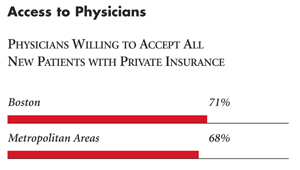

Boston Consumers’ Access to Care, 2001

Boston compared to metropolitan areas with over 200,000 population

| Unmet Need |

| PERSONS WHO DID NOT GET NEEDED MEDICAL CARE DURING THE LAST 12 MONTHS |

|

| Delayed Care |

| PERSONS WHO DELAYED GETTING NEEDED MEDICAL CARE DURING THE LAST 12 MONTHS |

|

| Out-of-Pocket Costs |

| PRIVATELY INSURED PEOPLE IN FAMILIES WITH ANNUAL OUT-OF-POCKET COSTS OF $500 OR MORE |

|

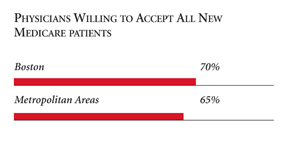

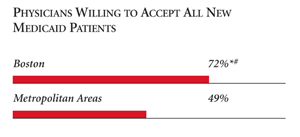

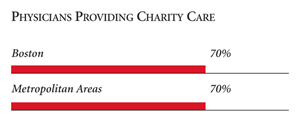

| Access to Physicians |

| PHYSICIANS WILLING TO ACCEPT ALL NEW PATIENTS WITH PRIVATE INSURANCE |

|

| PHYSICIANS WILLING TO ACCEPT ALL NEW MEDICARE PATIENTS |

|

| PHYSICIANS WILLING TO ACCEPT ALL NEW MEDICAID PATIENTS |

|

| PHYSICIANS PROVIDING CHARITY CARE |

|

| * Site value is significantly different from the mean for large

metropolitan areas over 200,000 population at p<.05. # Indicates a 12-site high. å Indicates a 12-site low. Source: HSC Community Tracking Study Household and Physician Surveys, 2000-01 Note: If a person reported both an unmet need and delayed care, that person is counted as having an unmet need only. Based on follow-up questions asking for reasons for unmet needs or delayed care, data include only responses where at least one of the reasons was related to the health care system. Responses related only to personal reasons were not considered as unmet need or delayed care. |

Background and Observations

| Boston Demographics | |

| Boston | Metropolitan Areas 200,000+ Population |

| Population1 4,550,463 |

|

| Persons Age 65 or Older2 | |

| 13% | 11% |

| Median Family Income2 | |

| $37,755 | $31,883 |

| Unemployment Rate3 | |

| 4.8% | 5.8%* |

| Persons Living in Poverty2 | |

| 8.2% | 12% |

| Persons Without Health Insurance2 | |

| 6.1% | 13% |

| Age-Adjusted Mortality Rate per 1,000 Population4 | |

| 8.0 | 8.8* |

* National average. Sources: |

|

| Health Care Utilization | |

| Boston | Metropolitan Areas 200,000+ Population |

| Adjusted Inpatient Admissions per 1,000 Population 1 | |

| 221 | 180 |

| Persons with Any Emergency Room Visit in Past Year 2 | |

| 21% | 19% |

| Persons with Any Doctor Visit in Past Year 2 | |

| 86% | 78% |

| Average Number of Surgeries in Past Year per 100 Persons 2 | |

| 20 | 17 |

| Sources: 1. American Hospital Association, 2000 2. HSC Community Tracking Study Household Survey, 2000-01 |

|

| Health System Characteristics | |

| Boston | Metropolitan Areas 200,000+ Population |

| Staffed Hospital Beds per 1,000 Population1 | |

| 2.3 | 2.5 |

| Physicians per 1,000 Population2 | |

| 2.7 | 1.9 |

| HMO Penetration, 19993 | |

| 48% | 38% |

| HMO Penetration, 20014 | |

| 41% | 37% |

| Medicare-Adjusted Average per Capita Cost (AAPCC) Rate, 20025 | |

| $635 | $575 |

| Sources: 1. American Hospital Association, 2000 2. Area Resource File, 2002 (includes nonfederal, patient care physicians, except radiologists, pathologists and anesthesiologists) 3. InterStudy Competitive Edge, 10.1 4. InterStudy Competitive Edge, 11.2 5. Centers for Medicare and Medicaid Services. Site estimate is payment rate for largest county in site; national estimate is national per capita spending on Medicare enrollees in Coordinated Care Plans in December 2002. |

|

The Community Tracking Study, the major effort of the Center for Studying Health System Change (HSC), tracks changes in the health system in 60 sites that are representative of the nation. HSC conducts surveys in all 60 communities every three years and site visits in 12 communities every two years. This Community Report series documents the findings from the fourth round of site visits. Analyses based on site visit and survey data from the Community Tracking Study are published by HSC in Issue Briefs, Tracking Reports, Data Bulletins and peer-reviewed journals. These publications are available at www.hschange.org.

Authors of the Boston Community Report:

John F. Hoadley, Georgetown University;

Debra A. Draper,

Mathematica Policy Research, Inc.; Sylvia Kuo, Mathematica Policy Research,

Inc.;

Peter J. Cunningham, HSC; Jessica Mittler, Mathematica Policy Research, Inc.;

Len M. Nichols, HSC;

Gloria J. Bazzoli, Virginia Commonwealth University;

Justin White, Mathematica

Policy Research, Inc.; Robert A. Berenson, AcademyHealth

Community Reports are published by HSC:

President: Paul B. Ginsburg

Director of Site Visits: Cara S. Lesser

Editor: The Stein Group

For additional copies or to be added to the mailing list, contact HSC at:

600 Maryland Avenue SW, Suite 550, Washington, DC 20024-2512

Tel: (202) 554-7549 (for publication information)

Tel: (202) 484-5261 (for general HSC information)

Fax: (202) 484-9258

www.hschange.org