Rough Passage: Affordable Health Coverage for Near-Elderly Americans

HSC Policy Analysis No. 2

September 2009

Ha T. Tu, Allison Liebhaber

Adequate and affordable insurance coverage is a particular concern for near-elderly Americans—those aged 55 to 64—because this group is at greater risk for serious health problems and high health care costs than younger adults. Moreover, because of their age and increased likelihood of health problems, the near elderly without access to employer-sponsored coverage often face problems obtaining affordable and adequate coverage in the individual insurance market. Among the policy options to expand coverage and improve affordability for the near elderly, comprehensive reform of the individual insurance market, combined with a Medicaid expansion for those with very low incomes, would be the most effective and far-reaching approach. Short of health reform, a subsidized Medicare buy-in program combined with a Medicaid expansion would be the most comprehensive approach. Other policy options are generally too incremental to make a substantial impact on near-elderly uninsurance, and options that rely exclusively on subsidizing employer-sponsored insurance risk excluding the near-elderly Americans most in need of help—those with low incomes and without health insurance.

- Special Policy Considerations Concering the Near Elderly

- A Closer Look a the Near Elderly

- Evaluation Policy Options

- Likely Impact of Health Reform

- Medicare Buy-In

- Tax Credits/Premium Subsidies

- Reinsurance

- Other Policy Options

- Conclusions and Implications

- Notes

- Data Source and Funding Acknowledgement

Special Policy Considerations Concerning the Near Elderly

![]() n 2007, approximately 33 million people, or 10.8 percent

of the U.S. population, were 55 to 64 years old.1 Overall,

this group, often referred to as the near elderly, is more likely than younger

adults to have health insurance: 12 percent of near-elderly adults, or 4 million

people, lacked health insurance, compared with 28 percent of adults aged 19-34

and 17 percent of adults aged 35-54.2 The uninsurance rate

for near-elderly people has remained steady at approximately 12 percent since

the mid-1990s, in contrast to rising uninsurance rates for younger adults3

(see box below for more about insurance trends).

n 2007, approximately 33 million people, or 10.8 percent

of the U.S. population, were 55 to 64 years old.1 Overall,

this group, often referred to as the near elderly, is more likely than younger

adults to have health insurance: 12 percent of near-elderly adults, or 4 million

people, lacked health insurance, compared with 28 percent of adults aged 19-34

and 17 percent of adults aged 35-54.2 The uninsurance rate

for near-elderly people has remained steady at approximately 12 percent since

the mid-1990s, in contrast to rising uninsurance rates for younger adults3

(see box below for more about insurance trends).

Despite relatively high and stable health insurance coverage rates, many experts believe that the near-elderly population merits attention from policy makers for three key reasons. First, the consequences of uninsurance tend to be much more serious for this group than for younger adults. The prevalence of chronic conditions and the risk of major acute illnesses increase markedly with age, so the uninsured near elderly face much greater financial risks than younger uninsured adults. Per capita medical expenditures are about 30 percent greater for the near elderly than for adults aged 45-54, and the likelihood of having very high expenditures (above $10,000) increases with age.10

The second issue is the quality of the insurance coverage available to this group. More than 3 million near-elderly Americans purchase health insurance in the individual market, where premiums are markedly higher because of adverse selection into the risk pool, higher administrative costs and the lack of employer subsidies. Because of the high cost of comprehensive coverage, many consumers in the individual market purchase policies with high deductibles and limited benefits. Even individuals who are able to afford the high cost of individual coverage may be denied coverage completely by insurers for health problems or a history of certain conditions.

Third, the relatively moderate and stable rate of uninsurance for the near elderly likely reflects the high priority that people in this age group place on having health coverage and may mask the substantial financial sacrifices that many are making to maintain coverage. The health insurance status of the near elderly also has implications for Medicare, since a growing uninsured population entering the program will result in higher costs. Indeed, previous research has shown that previously uninsured Medicare beneficiaries have more doctor visits, hospital stays and total medical expenditures than previously insured beneficiaries.11

Back to Top

Insurance Coverage Trends |

That there has been no decline in coverage rates for the near elderly over the past two decades may seem surprising given the declining availability of health benefits to early retirees (those under age 65) over the same period. Among all private-sector employers, for example, the proportion offering early-retiree health benefits declined from 22 percent in 1997 to 11 percent in 2008.4 The same downward trend is evident among large employers—those most likely to offer retiree benefits. Among companies with 1,000 or more workers, only 36 percent offered early-retiree health benefits in 2008, compared to 53 percent in 1997.5 The rising cost of health care has been a key factor in the declining availability of retiree health benefits. Another major factor was a 1990 rule change by the Financial Accounting Standards Board (FASB) that required employers to report as a liability on their books the entire cost of their unfunded retiree health obligation. Prior to this rule change, most employers had simply paid the annual cost of retiree health premiums out of their general budgets—an approach called pay-as-you-go accounting.6 Retiree health insurance offers dropped after the implementation of the FASB rule. The accounting rule change, together with the rising cost of providing retiree health benefits, means that most workers today will never become eligible for retiree health insurance. Among companies that still offer retiree coverage, many have tightened eligibility requirements and/or shifted a greater share of costs onto the retiree by capping employer contributions, either per person or globally. Some employers have eliminated their subsidy for retiree health benefits altogether, instituting “access-only” plans in which retirees must pay the full cost of the benefit. To date, public-sector employers have been much more likely than private companies of the same size to continue offering retiree health benefits. However, this is likely to change in the wake of Governmental Accounting Standards Board (GASB) rulings—similar to FASB’s earlier rulings—requiring public employers to report their full retiree health liability to taxpayers beginning in 2007.7 There are some key reasons why declining availability of retiree benefits has not led to greater uninsurance among the near-elderly population. First, most of the changes made by employers to retiree health benefits are more likely to apply to future retirees than current retirees. Second, people in this age group are remaining in the labor force longer, at least in part to maintain health insurance coverage. Previous research has found that workers are substantially less likely to retire if their employer-sponsored coverage does not continue until they reach age 65 than if their employers provide pre-Medicare retiree health benefits.8 Overall, the proportion of near-elderly people still active in the workforce increased from 63 percent in 1995 to 68 percent in 2007.9 Finally, because health insurance tends to be a high priority for the near elderly, many without access to employer-sponsored insurance seek coverage in the individual insurance market, despite high premiums and typically less comprehensive coverage than group insurance. |

A Closer Look at the Near Elderly

![]() revious research has shown that the near-elderly population

is a diverse group: 68 percent are still in the labor force, 15 percent are

retired, 11 percent are not working because of illness or disability, and the

rest engage in other activities, such as homemaking.12

The three main subgroups—working, retired, and ill or disabled—are strikingly

different from one another in health status, income and insurance coverage.

revious research has shown that the near-elderly population

is a diverse group: 68 percent are still in the labor force, 15 percent are

retired, 11 percent are not working because of illness or disability, and the

rest engage in other activities, such as homemaking.12

The three main subgroups—working, retired, and ill or disabled—are strikingly

different from one another in health status, income and insurance coverage.

Those who have retired tend to be in relatively good health; not surprisingly, those who do not work because of illness or disability are very likely to report fair or poor health.13 The remaining two-thirds of the near-elderly population—the non-retirees—are in much better health than the ill and disabled but somewhat worse health than the retirees.

Non-retirees fare the best financially with median family incomes 40 percent higher than those of retirees and more than three times those of the ill and disabled.14 Income and health are interrelated, as health problems can interfere with an individual’s ability to work and, therefore, cause income to decline.

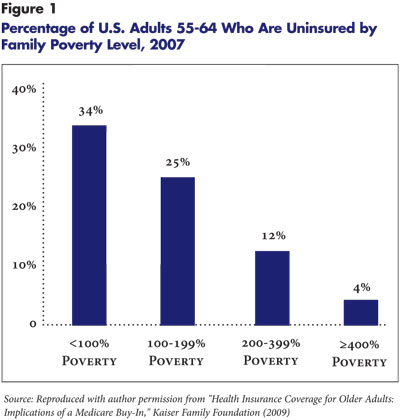

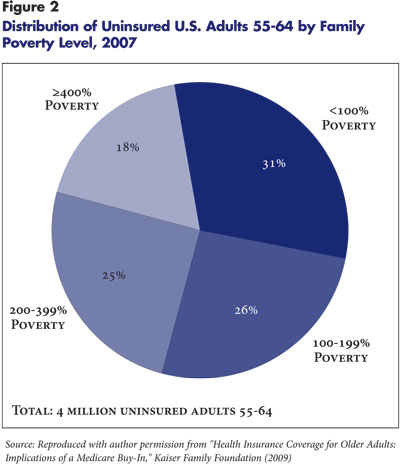

The prevalence of uninsurance tends to be relatively low (10%) for the ill and disabled because more than three-quarters of this group qualify for public insurance.15 Uninsurance rates are similarly low (11%) for non-retirees—about four in five have employer-based coverage. About 14 percent of early retirees lack health insurance. Within each of these groups, however, insurance rates vary greatly by income, with uninsurance rates strikingly higher for near-elderly individuals in the lowest income groups (see Figure 1 and Figure 2). Of the 4 million uninsured near elderly, about 2.3 million are low income—family incomes no higher than 200 percent of poverty, or $29,140 for a family of two in 2009—and another 1 million have modest to moderate incomes—family incomes between 200 percent and 400 percent of poverty.

Back to Top

|

|

Evaluating Policy Options

![]() n analyzing options for expanding insurance coverage and improving health care affordability to the near elderly, the following criteria can be used to assess the options:

n analyzing options for expanding insurance coverage and improving health care affordability to the near elderly, the following criteria can be used to assess the options:

- Efficiency: The extent to which tax dollars are put to optimal use, including considerations such as the following:

- The ability to pool risks and exploit administrative economies effectively.16

- The ability to minimize distortions such as labor-market effects (e.g., individual incentives regarding work and retirement) and crowd-out effects (the substitution of one form of insurance for another rather than an expansion of insurance overall).

- Equity: The extent to which the policy targets resources to those who need them most (in particular, those currently lacking insurance and those with the least ability to pay) and minimizes the provision of subsidies to those who can afford to pay for insurance.

Along with policies targeted at individuals, policy makers may also choose to focus on programs aimed at maintaining employer-based retiree health benefits. Although the number of near-elderly retirees receiving health benefits from a former employer is modest, this population represents a significant cost burden to some large employers and unions concentrated in certain industries, including the automobile, communications, utilities, mining and plastics industries.

Some experts argue that federal assistance to these employers is warranted, given the competitive disadvantage they face when they must compete against companies not burdened by legacy retiree benefits and/or with younger workforces. Some also argue that by subsidizing retiree benefits, government can encourage companies that still have these benefits to “stay in the game,” thereby helping to moderate community-rated premiums in a reformed individual insurance market by keeping as many expensive early retirees as possible out of the market.17 To the extent that government subsidies succeed in encouraging employers to “stay in the game,” near-elderly people with early-retiree coverage would also benefit from the retention of employer contributions toward their coverage.

Such views are far from universal, however, with some experts questioning whether it is equitable to ask taxpayers to subsidize retiree benefits for a particular segment of the near elderly when most taxpayers themselves do not have access to employer-sponsored retiree health benefits.

Back to Top

Likely Impact of Health Reform

![]() ny discussion of coverage options for the near elderly needs to be considered first in the context of comprehensive health reform—in particular expanding Medicaid coverage to childless adults and reforming the individual insurance market.

ny discussion of coverage options for the near elderly needs to be considered first in the context of comprehensive health reform—in particular expanding Medicaid coverage to childless adults and reforming the individual insurance market.

Major congressional proposals call for an expansion of Medicaid eligibility to all adults under age 65 with incomes below certain levels. For example, the House Tri-Committee bill (H.R. 3200) proposes expanding Medicaid to everyone with incomes up to 133 percent of poverty ($14,400 a year for an individual in 2009)—an approach that would benefit many of the most vulnerable among the near elderly. Approximately 5 million near-elderly people have incomes no higher than 133 percent of poverty, and about 1.6 million in this group are uninsured. If all 1.6 million people enrolled in Medicaid, that alone would slash the uninsurance rate for the near elderly from 12 percent to 7.2 percent.18

For higher-income, near-elderly people, purchasing coverage in the individual market is their only option if they lack access to employer-sponsored or public coverage. Currently, the individual market varies tremendously by state, with some states imposing minimal regulation while others have tried to improve access by mandating guaranteed issue and community rating, where an individual’s health status is not considered when setting premiums. In the latter states, affordability has emerged as a key barrier, as rising premiums drive younger, healthier individuals from the individual market, leaving a shrinking, unsustainable risk pool.

Massachusetts has been the only state to implement comprehensive health reform, using an individual mandate to help keep healthy individuals in the risk pool and merging the individual insurance market with the much larger small group market to improve stability.

While federal health reform options currently being discussed in Congress are in flux, many experts agree that a reform package will likely include the following elements:

A health insurance exchange. The concept behind an exchange is to create an organized marketplace where individuals and small employers can purchase insurance. The exchange likely would centralize and perform many different functions, such as facilitating enrollment, overseeing benefit standards to ensure that plans offer “meaningful” coverage, spreading risk across plans, and delivering premium subsidies to eligible enrollees. If an exchange is successful in lowering the costs of distributing insurance to individuals, it could lead to lower premiums.

The question of who will be allowed to buy into the exchange in addition to individuals is an important issue. An amendment to H.R. 3200, for example, limits group size to 15 employees in the first year of the exchange, 25 employees in the second year and 50 employees in the third year, with an option to allow eligibility for group sizes above 50, beginning in the third year.19

Some larger employers responsible for health benefits for early retirees or an older, less healthy workforce might find it advantageous to participate in the exchange if allowed to do so. To the extent that their participation raises community-rated premiums, it would increase the financial burden on other exchange participants, which in turn is likely to trigger other unintended outcomes—for example, forcing government to increase premium subsidies to lower-income participants and to deal with more financial hardship exemptions for other participants.

Guaranteed issue, guaranteed renewal and modified community rating for the individual and small group markets. Under modified community rating, premiums cannot vary by health status but may vary based on other characteristics. It is likely that premium variations will be allowed to vary by age, tobacco use, family composition and geography. The Senate Finance Committee chairman’s mark (September 2009) proposed a maximum age variation of 5:1, with an overall permissible variation, including factors in addition to age, of 7.5:1. The Senate Health, Education, Labor and Pensions (HELP) Committee bill and H.R. 3200 propose a much narrower age rate band of 2:1. Guaranteed issue, guaranteed renewal and modified community rating are of critical importance to the near elderly, many of whom are denied coverage in the individual market or are offered non-comprehensive policies at very high premiums. Moreover, to the extent that the exchange facilitates a broader risk pool, it benefits near-elderly enrollees, who are implicitly subsidized by younger, healthier enrollees through modified community rating.

Both the HELP bill and H.R. 3200 originally specified that guaranteed issue, guaranteed renewal and modified community rating would apply to all insured products—regardless of group size—inside and outside the exchange. An amendment to the HELP bill has since exempted large groups from the modified community rating requirement, though the definition of large group is still to be determined. If retained in a final version of health reform legislation, the requirement for modified community rating across all insured group products would benefit employers providing fully insured health benefits to early retirees and/or a disproportionate share of older active workers. However, in raising premiums for firms with younger, healthier workforces, this provision likely would motivate many small and mid-size firms to consider moving to self-insurance to avoid community-rated premiums, even though many such firms may lack sufficiently large risk pools or financial resources to make self-insurance a prudent choice.

A minimum benefit package. Most bills require that insurance products offered through the exchange include a wide range of benefits, including prescription drugs, maternity care, and mental health and substance abuse services. In addition, plans would be required to offer preventive services with little or no patient cost sharing. Plans likely would be prohibited from placing lifetime limits on coverage or annual limits on any benefits.

Overall, the House Tri-Committee bill proposes a minimum actuarial value—defined as the proportion of covered health care expenses paid by the health plan as opposed to the enrollee—of 70 percent for the lowest plan option, while the Senate HELP Committee bill proposes a 76 percent minimum actuarial value. Such provisions would ensure more comprehensive coverage than is generally available now in the individual market and would particularly benefit older enrollees, who are more likely to utilize services and to have pre-existing health conditions that currently are excluded from covered benefits under many individual policies. However, the more comprehensive the minimum benefit package, the higher premiums will be. This is true for all exchange participants, but particularly for near-elderly participants whose premiums are higher under modified community rating that varies with age. To keep premiums affordable for a comprehensive minimum benefit package, government subsidies will have to be substantial.

Risk adjustment across plans. Experts agree on the need to implement a risk-adjustment mechanism to correct for uneven risk distribution across health plans and to ensure that premiums reflect the average cost of medical care rather than the mix of healthy and sick enrollees in any given plan. If the health reform package includes a provision for risk adjustment, the exchange is likely to be given responsibility for carrying out risk adjustment, which involves levying a charge on plans with less than average actuarial risk and redistributing those payments to plans with higher than average actuarial risk. Risk adjustment benefits the near elderly by removing insurers’ incentives to avoid sicker, higher-cost enrollees. The methods to be used are still undetermined, and there is substantial debate about the accuracy and effectiveness of existing risk-adjustment methods.20

H.R. 3200 currently applies risk adjustment only to plans within the exchange—an approach that may lead insurers to continue using risk selection and risk segmentation. For example, insurers may be motivated to steer small groups with younger workforces or favorable claims histories to products with lower premiums outside the exchange, leaving a less viable risk pool and higher premiums within the exchange. Likely in anticipation of this problem, the Senate HELP bill currently requires risk adjustment to be carried out not only across plans in the gateways but also across smaller insured plans outside the gateways.21

Coverage mandate for individuals and “pay-or-play” requirement for employers. Any health reform package is likely to include a provision to levy an excise tax on most individuals who do not purchase health insurance, either through an employer or an individual plan. Employers above a certain size may be required to either offer their full-time employees insurance coverage or pay a tax—for example, H.R. 3200 proposes an 8 percent payroll tax. The coverage offered by employers will need to meet minimum benefit package requirements. The individual mandate is critical to the viability of a reformed individual insurance market and would strongly benefit the near elderly by keeping younger, healthier individuals in the risk pool, thereby helping to moderate premiums for older enrollees.

Income-based premium subsidies. Most health reform proposals include premium subsidies for low-income individuals in the form of refundable tax credits paid in advance. The specifics of proposals vary widely, with many providing sliding-scale subsidies for those with incomes up to 400 percent of poverty. Within eligible income ranges, some proposals cap an individual’s required premium contribution at a specified percentage of income (e.g., 10%).

Although age-specific premium subsidies are not under consideration, an approach of capping premiums to a percentage of income would be more beneficial to the near elderly than the alternative approach of fixed-dollar premium subsidies for each income level. This is especially true if premiums are allowed to vary by age by as much as 5 to 1. For example, if premiums were $100 a month for younger enrollees but $500 for near-elderly enrollees, a flat subsidy would cover a much smaller part of the premium for the older enrollees. With premiums capped at a percentage of income, the government would, in effect, be providing larger subsidies to older enrollees because the cost of their premiums as a percentage of income would be much higher. This approach would greatly improve the affordability of coverage for older enrollees whose incomes fall below the threshold but would raise the overall cost of the subsidies.

Experts generally agree that a reformed individual insurance market incorporating all the elements described above would offer by far the most promising approach for expanding coverage for the near elderly. However, concerns about the costs of the health reform package are causing congressional committees to reassess both income eligibility levels for subsidies and premium capping ratios. Some proposals now set 300 percent of poverty as the maximum income eligible for any subsidies and 15 percent of income as the maximum premium contribution expected of individuals. Clearly, the more stringent the income thresholds, the more difficult it will be to obtain affordable coverage on the exchange. This is particularly true for near-elderly individuals, who face substantially higher premiums, even under the proposals most favorable to them—those with 2:1 age-rate bands. Similarly, to the extent that other key reform elements such as risk adjustment or a minimum benefit package are diluted, the benefits to the near elderly will be reduced as well.

If individual insurance market reforms are implemented, they are likely to have some effects on the labor market, particularly among the near-elderly population. An unknown, but likely significant, number of people in this age group are currently in a job-lock situation, where they have remained with their current employers primarily to maintain health benefits. In a reformed market, some of these people may retire, switch to part-time status, move to an employer not offering health coverage or to self employment.

In addition to these market reforms, H.R. 3200 and the Senate HELP bill both propose to subsidize employers providing health benefits to retirees between 55 and 64 years of age. The subsidy takes the form of a reinsurance program, in which the federal government would pay 80 percent of all claims between $15,000 and $90,000 per year for each early retiree. The reinsurance program is proposed as a temporary measure until the exchange is up and running, but some experts suggest making such a program permanent to help prevent further erosion of retiree benefits. Beyond providing some financial relief to employers that continue to provide early-retiree benefits, some suggest that such a program may benefit the exchange and the system overall by keeping many high-cost individuals out of the individual market, thus lowering community-rated premiums for those in the exchange.

The central drawback to reinsurance is that it reduces incentives for the insurer (or self-insured employer) to exercise effective utilization and care management. Therefore, if providing financial relief to employers with a large retiree burden is a policy goal, a direct credit to employers—modeled on the Medicare Part D credit—would be a more efficient mechanism for achieving that goal.22 And, the potential benefit to the exchange—keeping some high-cost individuals in private group markets and out of the individual market—would apply to a direct employer credit as well as a reinsurance program.

If comprehensive health reform is not implemented, then there are incremental coverage expansions targeted at the near-elderly population that policy makers could consider. Several of these approaches are described below.

Back to Top

Medicare Buy-In

![]() Medicare buy-in is an approach to covering the near elderly

that has been examined since the Clinton administration. More recently, Senate

Finance Committee Chairman Max Baucus proposed a Medicare buy-in as a temporary

option until the establishment of a health insurance exchange as part of comprehensive

health reform.23 Comprehensive national health reform

may eliminate the need for a Medicare buy-in once it is implemented, but a buy-in

could also be implemented in conjunction with other reforms to improve affordability

of coverage, specifically for the near elderly. While public support for a Medicare

buy-in is high, with 76 percent of adults in 2009 reporting they supported a

Medicare buy-in,24 there are several policy details that

need to be considered in implementing a buy-in program.

Medicare buy-in is an approach to covering the near elderly

that has been examined since the Clinton administration. More recently, Senate

Finance Committee Chairman Max Baucus proposed a Medicare buy-in as a temporary

option until the establishment of a health insurance exchange as part of comprehensive

health reform.23 Comprehensive national health reform

may eliminate the need for a Medicare buy-in once it is implemented, but a buy-in

could also be implemented in conjunction with other reforms to improve affordability

of coverage, specifically for the near elderly. While public support for a Medicare

buy-in is high, with 76 percent of adults in 2009 reporting they supported a

Medicare buy-in,24 there are several policy details that

need to be considered in implementing a buy-in program.

One of the most appealing aspects of a Medicare buy-in is that it does not rely on the individual insurance market and can build on an already-established administrative entity. However, depending on how premiums are priced, a buy-in may be too expensive to make a significant impact on the uninsured near elderly. This would be particularly true if a Medicare buy-in must be budget neutral. In 2008, the Congressional Budget Office estimated that annual premiums for a budget-neutral buy-in would be $7,600 for an individual.25 Clinton administration proposals would have lowered the buy-in premium for those aged 55 to 64 but would have required some enrollees to pay an extra monthly amount beginning at age 65—in essence providing a loan. Even under those reduced premiums, previous research suggests that the effect of a Medicare buy-in would modestly expand coverage, because many near-elderly individuals who currently lack insurance are low income and are likely to find unsubsidized Medicare premiums unaffordable.26 And, many of those who enroll would be dropping more expensive private individual coverage in favor of Medicare.

Beyond having a limited impact on the number of uninsured, high premiums can also result in problems with adverse selection in a Medicare buy-in. Requiring participants to pay a premium that covers the costs of the program would discourage healthy people from participating and attract mostly those with serious health problems who are most likely to use health services. Adverse selection, and a resulting further increase in premiums, is a very serious problem that could face an unsubsidized Medicare buy-in.

A buy-in program that utilized premium subsidies to lower the cost to participants would help to avoid problems of adverse selection and would further reduce the uninsurance rate. To get low-income people—the majority of the uninsured in the near-elderly group—to participate, income-related subsidies would have to be provided. However, premium subsidies, particularly depending on how generous they are and up to what income level they are provided, would increase the overall cost of the program to the federal government.

Although a Medicare buy-in without substantial subsidies would have a limited impact on the number of uninsured, it is important to look beyond uninsured numbers when estimating the effect of a buy-in. Many Medicare buy-in participants would be migrating into the program from the individual insurance market. As the individual market is currently structured, it is difficult for the near elderly to find coverage, and when they can find coverage, it is often extremely expensive and not very comprehensive. A Medicare buy-in would improve the availability, affordability and quality of coverage for those near elderly currently purchasing insurance in the individual market, although Medicare-only coverage (without supplemental Medigap insurance) may not be as comprehensive as some employer-sponsored policies.

There are several other issues to consider in the design of a Medicare buy-in. While some proposals would make a Medicare buy-in open to individuals 55 to 64, others restrict eligibility to individuals aged 62 to 64. One policy option would be to open the buy-in to the entire age group (ages 55-64) but with more restrictive eligibility criteria or higher premiums for the younger cohort. A second question about eligibility for a Medicare buy-in would be whether to allow those with access to employer-sponsored insurance to participate. Most proposals would restrict eligibility to those without access to a group health plan, mostly to prevent crowding out employer-sponsored insurance.

An attractive buy-in program might induce some employers to drop retiree coverage for those under age 65. To limit that, the Medicare buy-in could be opened to those with access to employer-sponsored benefits and a credit could be provided to employers to discourage them from dropping early-retiree coverage. This approach would be similar to the decision by policy makers to provide a credit to employers who maintained retiree prescription drug coverage after the Medicare Part D benefit took effect.

The benefit package is another consideration in designing a Medicare buy-in program. There appears to be little reason not to allow buy-in participants the full range of Medicare options—both fee-for-service and Medicare Advantage—and the full range of benefits. Policy makers also would need to consider whether to allow buy-in participants enrolling in traditional fee-for-service Medicare access to Medigap coverage, which limits out-of-pocket costs for care. When Medicare Part D legislation was authorized, awareness of how Medigap coverage increases the cost of Medicare caused lawmakers to prohibit supplementation. A similar approach of banning Medigap coverage for a Medicare buy-in is likely.

Another important factor in considering a Medicare buy-in is the effects that such a program would have on the labor market. While there is evidence that retirement decisions are affected by the presence of available health benefits, the impact of a Medicare buy-in on retirement decisions would largely depend on how the buy-in is priced. If premiums are designed to cover the costs of the program, they would still be priced higher than the benefits package most employees receive as active workers, and, in many cases, the benefits package for a buy-in would be less comprehensive. In fact, previous analysis suggests negligible effects on retirement decisions even under a moderately priced buy-in.27 While a buy-in could be an incentive to employers to drop retiree coverage, the number of employers still providing those benefits—particularly to active workers—continues to dwindle even in the absence of a buy-in. This effect could also be minimized by the provision of an employer credit.

Back to Top

Tax Credits/Premium Subsidies

![]() ax credits aimed at making health insurance more affordable to near-elderly individuals with low to moderate incomes need to be considered in combination with either comprehensive insurance market reform or a Medicare buy-in program. In the absence of either comprehensive reform or a Medicare buy-in, subsidies to near-elderly individuals to purchase in the individual market are likely to have little impact, as they would not address problems of adverse selection, coverage denials and pre-existing condition exclusions often faced by the near elderly.

ax credits aimed at making health insurance more affordable to near-elderly individuals with low to moderate incomes need to be considered in combination with either comprehensive insurance market reform or a Medicare buy-in program. In the absence of either comprehensive reform or a Medicare buy-in, subsidies to near-elderly individuals to purchase in the individual market are likely to have little impact, as they would not address problems of adverse selection, coverage denials and pre-existing condition exclusions often faced by the near elderly.

In the past, many variations of tax credits have been proposed to help pay for health coverage. Most proposals have involved tax credits aimed at subsidizing purchase of insurance in the individual market. These proposals have been widely criticized on several dimensions. The amount of most tax credits has been considered too small to make a serious impact on uninsurance.28 In addition, this approach might result in some movement from employer-sponsored insurance to individual insurance, if some employers drop coverage in response to the tax credits. Also, in the absence of individual insurance market reform, the reliance on this market would be a particular challenge for the near elderly, who would be more likely to confront such barriers as coverage denials and pre-existing condition exclusions. And, it remains difficult to structure the subsidy to be available to low-income individuals at the time they pay their premiums rather than at the end of the tax year. Without credits paid in advance, most low-income people cannot afford full upfront premium payments. The administrative costs of delivering subsidies in a nongroup setting can be very high, as evidenced by experience with the Health Coverage Tax Credit (HCTC) (see box on below for more information).

In contrast to the cumbersome HCTC mechanism for delivering subsidies, an efficient method would require centralizing the eligibility determination and the process for making subsidy payments into a single organization, such as an exchange. Administrative costs would be lower, and subsidy delivery more efficient, if the exchange is given the authority to standardize plans, limit the number of insurers, and reduce the number of transactions.35 The Massachusetts experience can be regarded as a model of streamlined “one-stop shopping,” where residents fill out a single common application for assistance; once their eligibility is determined, those qualifying for assistance are directed either to Medicaid or one of the subsidized plans offered through the state’s insurance exchange, the Connector.36

In the past, tax credits also have been proposed for use with employer-sponsored insurance. None of these proposals have targeted the near-elderly population specifically, but many have targeted workers below certain income levels (e.g., 200% of poverty). Providing substantial tax credits would help improve affordability to the estimated 12 percent of near-elderly people with incomes below 200 percent of poverty who currently have employer coverage but may be struggling to pay their share of premiums. Substantial subsidies also could help to cover many of the 4 percent of near-elderly people with incomes below 200 percent of poverty who currently decline employer coverage.37 However, this approach would not address the problems of the much larger group of low-income near elderly—more than four in five—who do not have access to employer coverage in the first place.

Back to Top

Health Coverage Tax Credit |

|

The HCTC program, established as part of the Trade Act of 2002, pays part of the health insurance premiums for workers displaced by trade and early retirees receiving payments from the Pension Benefit Guaranty Corporation (PBGC) and their families. It is the only program currently using federal income tax credits to subsidize health insurance coverage for people who might otherwise be uninsured.29 Some have suggested using an expanded version of the HCTC program as a mechanism for administering premium subsidies to near-elderly individuals. An Urban Institute analysis, however, indicates that the HCTC program has been administratively cumbersome and expensive to administer: 34 percent of total spending on the program can be attributed to the costs of administering the subsidy to eligible individuals.30 The high administrative costs stem primarily from the many monthly transactions that the Internal Revenue Service (IRS) must undertake with each enrollee and his or her health plan. Apart from IRS transactions, a portion of each premium paid to a participating health plan covers the plan’s administrative costs, which are particularly high for individual coverage.31 The HCTC experience suggests that using tax credits to individuals in larger reform efforts would create considerable inefficiency unless administrative costs can be substantially reduced by achieving economies of scale and streamlining the required number of transactions.32 In an employer context, there have been isolated but promising examples of a more efficient implementation of HCTCs. For example, when US Airways declared bankruptcy in 2005, its retirees aged 55 to 64 became eligible for HCTCs as a result of the company terminating its retiree health coverage and the PBGC taking over the company’s pension funds.33 US Airways was able to negotiate with the federal government to have the Treasury Department pay the 65 percent federal premium subsidy directly to the health plan each month, thereby making the subsidy payment “almost a seamless conversion” for the health plan.34 The US Airways experience may prove a useful model for other employers entering bankruptcy and wishing to provide as painless a transition for their retirees as possible in continuing their health care coverage. However, the applicability of this model is currently limited by the requirement that companies in bankruptcy must first have their pension plans taken over by the PBGC before their early retirees can become eligible for the HCTC program. A policy change allowing HCTC eligibility for early retirees whose companies either meet certain indicators of significant financial distress or declare bankruptcy but maintain their pension plans may merit consideration. |

Reinsurance

![]() arious government reinsurance options have been proposed

in the individual and small group health insurance markets. The key notion behind

government reinsurance in these markets is that much of the variation in expenditures

and financial risk faced by private insurers comes from having an unpredictable

number of high-cost cases in their risk pools. With government assuming much

of the responsibility for high-cost cases, private insurance markets would be

stabilized, insurers would have reduced incentive to avoid adverse selection,

and premiums would be expected to fall.38

arious government reinsurance options have been proposed

in the individual and small group health insurance markets. The key notion behind

government reinsurance in these markets is that much of the variation in expenditures

and financial risk faced by private insurers comes from having an unpredictable

number of high-cost cases in their risk pools. With government assuming much

of the responsibility for high-cost cases, private insurance markets would be

stabilized, insurers would have reduced incentive to avoid adverse selection,

and premiums would be expected to fall.38

None of the major House or Senate health reform proposals includes a provision for government reinsurance in the individual and small group markets on a permanent basis. One of the primary reasons is the high price tag. To substantially reduce risk variation (and ultimately premiums) in the individual market, previous research suggests that two program elements would be needed: (1) low thresholds (“attachment points”) of $15,000 to $30,000 per year, at which reinsurance would take effect, rather than the $50,000 or $100,000 in many previous policy proposals; and (2) government taking on a “full buy-out” (i.e., paying all costs from the first dollar for high-cost cases, not just the portion above the threshold).39 Such a program would not be viable because of an extremely high price tag and the complete removal of incentives for insurers (and enrollees) to control utilization. More modest reinsurance proposals—with higher thresholds and reinsurance only above the threshold—would have less ability to stabilize and reduce premiums in the individual and small group markets.

Overall, the key argument against government reinsurance is that it reduces the insurer’s incentive to manage care for enrollees effectively, and no substitute effort by government is envisioned in terms of utilization control and care management—probably for good reason, as the administrative burdens and costs of a reinsurance program would escalate dramatically if government were to take on direct responsibility for care management. The major objective of reinsurance—reducing the potential for adverse selection in the individual and small group markets—can be dealt with much more efficiently in the context of comprehensive market reform through mechanisms such as standardization of insurance products and risk adjustment across health plans.

Government reinsurance has also been proposed in a different context: to help subsidize early-retiree benefits. The earlier section on health reform discussed reinsurance programs included in health reform packages proposed by H.R. 3200 and the Senate HELP Committee. If health reform does not come to pass, such a reinsurance program still could be implemented as a standalone policy option. However, as noted earlier, a direct credit to employers for early-retiree coverage (similar to the Medicare Part D credit) would be a more efficient mechanism for subsidizing these employers, as it would not distort incentives for managing care.

Back to Top

Other Policy Options

![]() here are other, more incremental policies that have been put forward as options for expanding coverage for the near elderly. These options include:

here are other, more incremental policies that have been put forward as options for expanding coverage for the near elderly. These options include:

COBRA Expansions. Under the provisions of the Consolidated Omnibus Budget Reconciliation Act (COBRA) of 1986, most employees who leave a company can remain on their former company’s group health coverage for up to 18 months if they pay the full group rate plus a 2 percent administrative fee. Policy makers have considered several proposals for extending COBRA coverage for near-elderly individuals until they become eligible for Medicare at age 65. Such proposals have met with strong resistance from employers, who note that they already lose money under current COBRA provisions, since the average cost for providing COBRA coverage to former employees can range from 50 to 70 percent above the group rate, mostly because of adverse selection, according to some estimates cited by experts. In effect, employers and their active workers are providing substantial subsidies to former employees covered by COBRA. A COBRA expansion mandate limited to the near elderly would be even more expensive on a per capita basis for former employers and their active workers.

According to experts, employers would only accept COBRA extension mandates for the near elderly if they are allowed to charge COBRA premiums that reflect the full costs of the COBRA cohort rather than those of active workers. Such an approach, however, would raise COBRA premiums to such a level that adverse selection would worsen and take up by former employees likely would be low, unless government subsidies made up the difference. Government targeting of subsidies only to those eligible for COBRA might be regarded as inequitable, since many of the near elderly with low incomes and without health insurance do not have access to COBRA coverage.

Expansion of Tax-Advantaged Savings Vehicles. Some benefits consultants and other experts advocate changes to the tax code to facilitate the prefunding of health care for elderly and near-elderly individuals, either through an expansion of existing tax-advantaged savings accounts (such as health savings accounts) or the creation of new tax-advantaged retiree health savings accounts modeled after 401(k) retirement plans. Another policy proposal would allow individuals to make pre-tax withdrawals from their pension and 401(k) accounts for health care expenditures. Yet another approach would change tax laws governing tax-free trusts known as Voluntary Employees’ Beneficiary Associations (VEBAs), either allowing pre-tax individual contributions to VEBAs or increasing the tax-exempt limits for non-unionized employers’ contributions to VEBAs,40 or both.

Many benefits consultants advocate such tax-advantaged account expansions, noting that many employers who are not in a position to fund burdensome defined-benefit retiree health benefits would be interested in making tax-free defined contributions, in predictable and manageable amounts, to help prefund health benefits in the same way that they are prefunding retirement savings through 401(k) contributions. However, other experts noted that the federal tax dollars foregone in the creation and expansion of such tax-advantaged savings vehicles would tend to be redistributed disproportionately to higher-income individuals, because employers in high-wage sectors are more likely to offer such accounts and contribute generously to them, and high-wage workers are also much more likely to make sizable contributions to their own accounts. As a short-term strategy, the use of tax-advantaged savings vehicles is unlikely to have a measurable impact on the most vulnerable of the near elderly—the low-income uninsured. Longer term, it remains to be seen whether these tax-advantaged prefunding mechanisms can generate sufficient savings on behalf of enough low-income and moderate-income workers that their chances of becoming uninsured in their near-elderly years can be significantly reduced.

Federal Support of State High-Risk Pools. Thirty-five states currently have high-risk pools aimed at providing a private insurance option to people who cannot purchase private coverage because of their health status. State funding constraints have resulted in most high-risk pools offering limited benefits and requiring high premiums and large deductibles, and few providing subsidies to low-income enrollees.41 The Trade Act of 2002 provided federal funds for state high-risk pools, but most states used these federal funds to replace rather than supplement existing state funding sources.42

Policy analysts have suggested that a stronger commitment from the federal government—more funding, combined with uniform requirements for eligibility, benefits and income-based subsidies—could improve the ability of state high-risk pools to serve those with high medical needs and low to moderate incomes.43 However, the disadvantage of using a high-risk pool to provide coverage for a group such as the near elderly is that this mechanism maximizes the public dollars necessary to finance coverage for this group.44 Since they are segregated into their own risk pools by design, the expenses of high-cost enrollees cannot be spread across premiums charged to a broader population that includes younger, lower-risk individuals—as they would be under comprehensive reform of the individual insurance market. It is likely to be more politically challenging to adequately finance high-risk pools explicitly with public dollars than to spread costs of the high-risk population through privately paid premiums.45

Back to Top

Conclusions and Implications

![]() espite their relatively high insurance coverage rates, a strong argument can be made that Americans in the 55-64 age group merit special attention from policy makers given the much higher risks of serious health problems and resulting financial hardship that they face compared to younger Americans. If policy makers wish to expand insurance coverage and improve affordability of health care for near-elderly people, by far the most effective and efficient approach would be comprehensive health reform, encompassing not only individual insurance market reforms—including an individual mandate, guaranteed issue, modified community rating, risk adjustment across plans and income-based subsidies—but also a Medicaid expansion to provide coverage for the lowest-income individuals. As noted earlier, an expansion of Medicaid eligibility to all adults with incomes at or below 133 percent of poverty would have a powerful impact on coverage for the near-elderly—reducing their uninsurance rate from 12 percent to 7.2 percent, if all eligible people could be successfully enrolled.

espite their relatively high insurance coverage rates, a strong argument can be made that Americans in the 55-64 age group merit special attention from policy makers given the much higher risks of serious health problems and resulting financial hardship that they face compared to younger Americans. If policy makers wish to expand insurance coverage and improve affordability of health care for near-elderly people, by far the most effective and efficient approach would be comprehensive health reform, encompassing not only individual insurance market reforms—including an individual mandate, guaranteed issue, modified community rating, risk adjustment across plans and income-based subsidies—but also a Medicaid expansion to provide coverage for the lowest-income individuals. As noted earlier, an expansion of Medicaid eligibility to all adults with incomes at or below 133 percent of poverty would have a powerful impact on coverage for the near-elderly—reducing their uninsurance rate from 12 percent to 7.2 percent, if all eligible people could be successfully enrolled.

If health reform fails to become a reality, then the most far-reaching approach would be a Medicare buy-in program with substantial subsidies, combined with a Medicaid expansion for the lowest-income individuals. This approach would have the advantage of relying on established programs rather than building new systems entirely. Some policy makers have proposed a Medicare buy-in designed to be budget neutral. This would help near-elderly individuals previously insured in the individual market, but the high premiums required by such an approach would mean that few previously uninsured people would gain coverage. In addition, adverse selection would be a serious problem in a Medicare buy-in without substantial subsidies.

Any comprehensive approach that makes a substantial impact on coverage and affordability is certain to carry a very high price tag, because the health status of near-elderly Americans makes them an expensive group to insure. Without sizable premium subsidies, neither reform of the individual market nor an expansion of Medicare eligibility would be sufficient to make a significant dent in the proportion of uninsured near-elderly people.

Other policy options have been proposed but are more incremental in nature—therefore limited in their expected impact—and often do not target the near elderly who are most in need of help. For example, options such as subsidies for COBRA coverage and expansions of tax-preferred accounts tend to help the relatively advantaged more than the most vulnerable among the near elderly. Approaches aimed at improving affordability of individual insurance—using mechanisms such as tax credits and reinsurance—would have little impact in the absence of comprehensive reform to the individual insurance market and are more likely to provide financial relief to those already covered in this market—including higher-income people—than to expand coverage to the uninsured.

If policy makers wish to focus on options for preventing further erosion of health benefits to early retirees, the most direct and efficient mechanism would likely be a tax credit to employers who provide early-retiree health benefits—similar to the Medicare Part D credit paid to employers who maintain retiree prescription drug coverage. Government reinsurance of retiree coverage has been proposed as an alternative mechanism, but because reinsurance reduces the insurer’s incentive to manage care, it is likely to prove a less efficient approach to subsidizing coverage than direct tax credits to employers.

Back to Top

Notes

Back to Top

Data Source and Funding Acknowledgement

To examine policy options for the near elderly, HSC researchers conducted a review of the existing literature. In addition, interviews were conducted with select thought leaders and experts on this topic. These experts included benefits consultants, researchers and policy analysts. All interviews were conducted by a two-person interview team between May and June 2009.

Funding Acknowledgement: This policy analysis was supported by the National Institute for Health Care Reform.

Back to Top

POLICY PERSPECTIVES are published by the Center for Studying Health

System Change.

600 Maryland Avenue, SW, Suite 550

Washington, DC 20024-2512

Tel: (202) 484-5261

Fax: (202) 484-9258

www.hschange.org